I have written a few times why comparing valuation metrics for the U.S. equity market and most others around the world is a futile exercise, mainly because the U.S. market is significantly different in terms of its sector composition, and furthermore because global sector compositions are vastly different by region and industry.

Without repeating those arguments here, I wanted to illustrate my point in a different fashion, and that is by charting a historical comparison of the U.S. and European equity markets versus global growth and value indices. By doing so, I hope to illustrate the evolution of the U.S. equity market from a more balanced to a growth-oriented market, while showing, by way of comparison, that the broader European market has historically been, – and remains even now, – an equity market with a value tilt.

In the first example, it can clearly be seen that the European market, – which is heavily weighted in classic value-sectors such as banks and energy, has historically had a very high correlation with the global value index, as judged by their respective MSCI indices. Indeed, the correlation of the three-year rolling returns for the two indices is greater than 90% over more than four decades, and more than 95% since 2000:

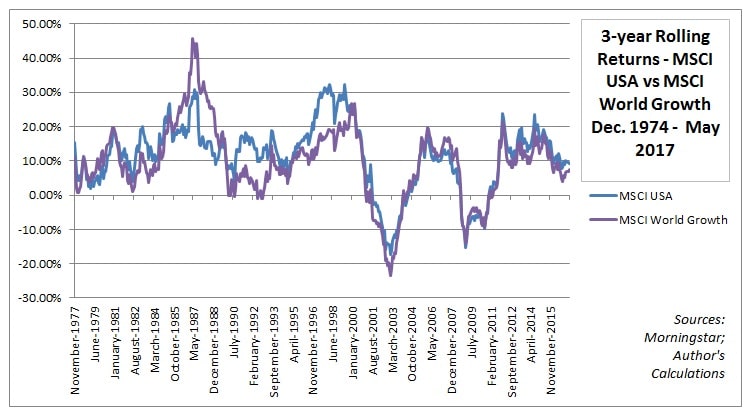

In contrast, the U.S. market, now dominated by classic growth sectors such as technology and healthcare, has transformed itself into a de facto growth fund. Importantly, while correlation for the three-year rolling returns of the MSCI USA index and the MSCI World Growth index is only 84% since 1974, it is greater than 96% since 2000:

Valuation metrics, when comparing similarly composed indices, confirm this development. Valuations are very similar not just for the broad European market and the global value portfolio, but also for the U.S. value portfolio:

The situation is much the same for the broad U.S. market and the global growth portfolio, and also for the European basket of growth-oriented stocks:

This is yet more evidence that over the last twenty years or so, something significant has changed within the U.S. equity markets in terms of composition, thus making once simple comparisons between global markets substantially more difficult, all the while causing consternation among those like Jeremy Grantham, who have been forced to admit that the mean reversion of equity valuations for which they have so long been calling may be later still in coming, if indeed it comes at all.

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.