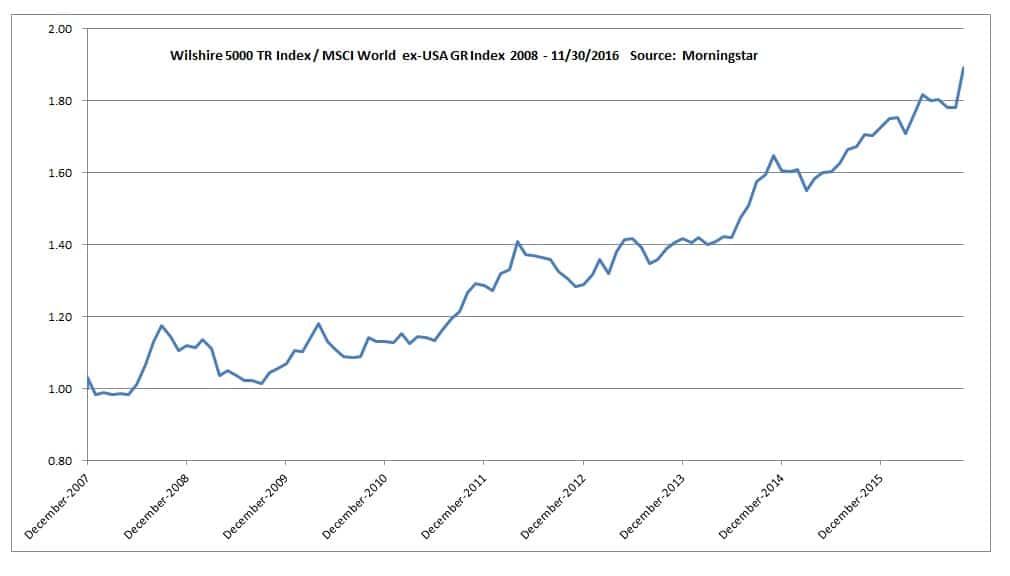

Over the last several years, American investors who have diversified their portfolios to include foreign equities have dealt with a significant underperformance of their foreign holdings relative to their domestic stock holdings. As you can see from the chart below, since 2008, it has been a very one-sided affair for the US versus the rest of the world, as the MSCI World ex-USA index “returned” an annualized -.22% over this period, while the American index, the Wilshire 5000, returned greater than 7% annualized:

As a result of this lackluster performance, it is likely that many have been tempted to dump their foreign positions from their portfolios. In a post from November titled “Keep the Faith,” Jonathan Clements wrote that to abandon all foreign investments would be a mistake, based on the historical evidence:

“At first blush, foreign stocks look like a dubious choice, returning 7.9% a year over the past nine decades, versus 9.8% for the S&P 500. But that huge performance gap was driven in large part by the 1940s, when some foreign markets were devastated by the Second World War, and by the 1990s, when the U.S. market was driven to giddy heights by the technology boom. Foreign stocks lagged behind the U.S. market by 13.9 percentage points a year in the 1940s and by 11.1 points in the 1990s.

What if you look at the other six full decades depicted in the chart? There was only one decade—the 1960s—when U.S. stocks outpaced foreign shares. Indeed, foreign shares occasionally proved to be a great diversifier for U.S. stocks, notably in the wretched 1970s, when foreign markets scored 10.1% a year, while U.S. stocks eked out an inflation-lagging 5.8%.”

While I happen to agree with Mr. Clements on this point, I think investors would be less prone to abandoning foreign equities if they understood the basic relationship between foreign equities and the variation in the value of the US dollar, as well as the diversification benefits foreign equities bring to a portfolio. If we revisit the chart from above, we can see that the dramatic outperformance of the US versus the world since 2008 has largely coincided with a surge in the US dollar versus other major currencies:

For those wondering why the US dollar should have such a large impact on the difference in returns between domestic and foreign shares, here is a brief explanation. Essentially, almost all US investors are going to have dollar-denominated assets in their portfolios, be they shares of American corporations such as Apple and Ford, or ADRs (American depositary receipts) of foreign companies, such as BMW or Toyota. Because ADRs are denominated in dollars, they are subject not only to the natural volatility of the markets, but also to the fluctuation of the exchange rate between their home currency and the dollar. While it is true that American multinationals also face additional volatility from currency fluctuation (a stronger dollar means that their products are less competitive, and that may hurt their bottom lines), the impact is greater overall on ADRs. We can observe this by comparing the relative performance of two major multinationals, the US company, Colgate-Palmolive, and the Swiss company, Nestle (via its USD-denominated ADR returns). Even though Nestle returned 14.11% per year and Colgate-Palmolive only 12.4% over this time frame, the periods of Colgate’s superior returns were largely tied to USD strength:

This relationship between foreign shares and the dollar also works in reverse: when the dollar is weak, foreign equities should outperform American equities as earnings and dividends denominated in appreciating (versus the dollar) currencies are translated into less valuable dollars (and thus buy more). This can be illustrated easily enough using the example Mr. Clements gave us of the 1970s. Since Federal Reserve (FRED) data for the dollar go back only to the beginning of 1973, I compared the MSCI World ex-USA GR index versus the Wilshire 5000 total-return index from 1973-1979, and charted the relative performance versus the dollar. Over this time period, the dollar index declined about 11%, while the MSCI World ex-USA index averaged 8.2% per year, versus 4.56% for the Wilshire:

Certainly, these are small sample sizes, but the relationship holds over much longer periods:

However, it should be noted that the impact of the dollar varies on a country to country basis. Consider the difference in relative performance between the Dow Jones Switzerland TR index versus the S&P 500, and relative performance of the Dow Jones Brazil Index versus the S&P. First, Switzerland:

And then Brazil:

That dollar-denominated Swiss equities should be less susceptible to swings in the dollar is not surprising; the Swiss currency, the franc, has been much more stable versus the world’s major currencies, so dramatic swings against the dollar have been, and should remain, unlikely. Brazil, on the other hand, is an emerging market with a history of major inflation, and its currency, the real, is prone to major swings. This is true of many other emerging market nations, which, like Brazil, have economies that are heavily correlated with commodities, and commodities themselves are very sensitive to dollar strength. Investors in countries like Brazil that are especially sensitive to dollar fluctuations should be prepared to expect magnified outcomes, both positive and negative.

The point of all this is that the negative correlation between foreign equities and the dollar is, to borrow Matt Levine’s phrase, ‘a feature, not a bug,’ as it makes foreign equities great portfolio diversifiers. As such, investors should be prepared to understand that extended periods of underperformance are likely in a world of floating exchange rates as currencies have cycles of strength and weakness all their own. It should also be considered that, in the years since the financial crisis, the effect of unprecedented central bank policies on global currencies may have affected the duration and depth of currency cycles, and therefore also the relative performance of US and foreign equities, so investing abroad may require more discipline and patience than it required previously.

When assembling a portfolio of foreign equities, investors should carefully consider that not all equity markets are the same, and that they should diversify their foreign equity holdings across many different countries, currencies, and sectors to reap the full benefit of investing abroad, while attempting to smooth the negative impacts of strong dollar cycles. What is more, while currency hedging foreign equity exposure (that is, making your foreign positions trade more like domestic shares by reducing the currency part of the equation) has gained in popularity during this recent cycle of dollar strength, previous cycles show that that might be a mistake as there can also be extended periods of dollar weakness, and thus weaker portfolio performance overall during these cycles:

Thanks, as always, to my friend, Jake, at EconomPic Data, for his help with the graphics.

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.