For several years now, many financial commentators have remarked on how elevated valuation multiples are for US stocks. Many have noted that US stocks appear especially expensive when compared to what investors would pay for stocks in other markets around the globe.

However, to some extent, comparing the US with other stock markets from around the world is somewhat like comparing apples and oranges. The US is a particularly dynamic market, and sector leadership varies from year to year, so context is crucial in terms of gauging valuations. Some might be tempted to look at rich valuations in the US compared to the rest of the developed world or emerging markets and think that those are relative bargains, assuming that all stock markets are essentially the same (they are not). In fact, a closer look at the composition of the US market versus the rest of the world’s major markets may be informative as to just why US valuations have remained elevated above historical averages for so long, and why waiting for “cheap” markets such as Europe to narrow the gap with the US valuation-wise may be foolish.

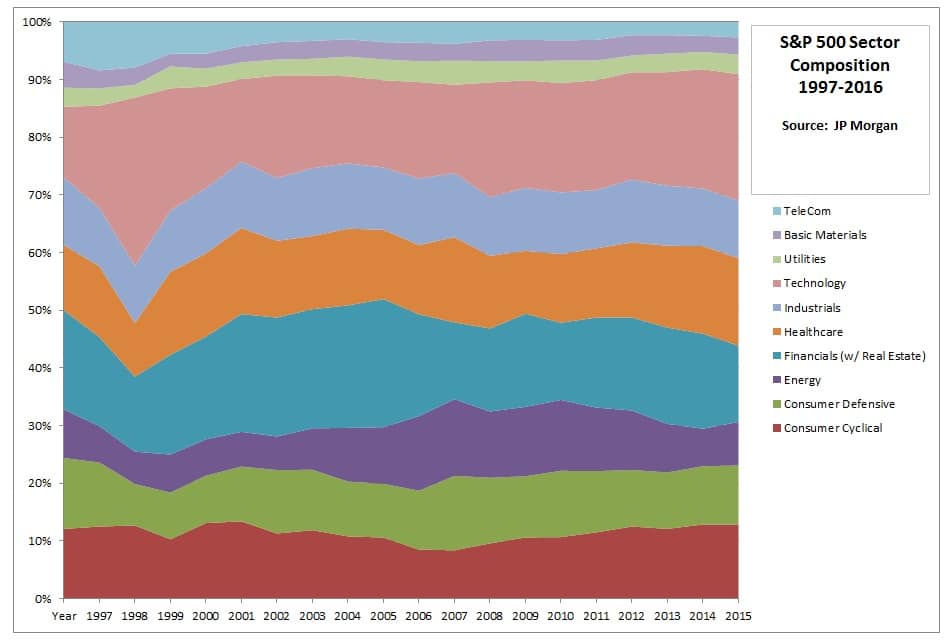

First of all, let’s examine the sector composition of the S&P 500 over the last 20 years:

You can see from the chart above that the US market has come to be dominated by sectors with a history of higher-than-average valuations as 62% of the US market is currently consumer discretionary, consumer staples, healthcare, telecommunications, and IT.

Conversely, when we look at the major index for the developed world, the MSCI EAFE (Europe, Asia, Far East), we can see that the sector composition is substantially different:

We can tell from this chart that the EAFE index is largely dominated by sectors with a history of lower-than-average valuations: financials, industrials, energy, utilities, and materials.

The difference in market composition is even greater when comparing “cheap” emerging markets with the US. We can see from the chart below that EM composition is almost the direct opposite of the US as the historically low-valuation sectors make up roughly three-fifths of the market:

While we don’t have specific sector valuation data, we can approximate ex-US valuations using the pertinent State Street ETF data. (Note: For this exercise, I swapped out the EAFE index for the MSCI World ex-USA index as it would more closely match the State Street ETF data. Also, I elected to exclude real estate from this example as price-to-earnings may not be the best valuation method for that sector.)

Using these inputs, and multiplying the MSCI World ex-USA weights by the State Street ex-USA sector ETF P/E data, we can approximate a forward price-to-earnings (that is, based on the current price of sector divided by next year’s forecasted earnings), for the world ex-USA. The US is indeed more expensive than the rest of the world, but not substantially so [Note: Sector weightings were re-weighted to account for no real estate sector representation.]:

In fact, if the MSCI World ex-USA index carried the same industry weights as the S&P 500, its forward P/E would be about 17.44, which is fairly close to the S&P’s actual forward P/E, whereas if we reverse it and apply the MSCI World ex-USA weights to the S&P 500, the forward P/E would be slightly lower at 17.58. In other words, by adjusting for sector weightings, we can see that regional valuations aren’t all that different.

To be sure, there are other indications such as the cyclically-adjusted price-to-earnings ratio, or “CAPE” (also known as Shilller P/E) that show a greater disparity in valuations between the US and many other markets around the world, particularly in emerging markets such as Brazil and Russia. But, as Philosophical Economics pointed out, digging a little deeper into the low-CAPE markets reveals much the same thing: the cheapest markets by CAPE tend to be those dominated “low-valuation” industries such as energy and financials.

The takeaway here is that US stocks aren’t cheap, but a case can be made that the US is not substantially more expensive than the rest of the world when looking at it through the lens of sector composition. Furthermore, the cheapest markets in the world are cheap for a reason, be it because they are dominated by low-valuation sectors, high inflation, etc. Investors should always diversify their portfolios abroad, and it would be wise to prepare for muted returns in the US going forward. However, using valuation as a reason to abandon the US altogether would be a mistake as it is by no means clear that, on a sector by sector basis, better bargains are to be had overseas.

For further reading:

Star Capital’s report on the same topic

http://www.starcapital.de/docs/2015-04_Sector_Adjusted_Country_Valuation_Keimling.pdf

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.