In “Relative Equity Valuations, Diversification, and Creative Destruction,” I discussed how market dynamism – the continual churn of equity market components – affects investor confidence and underpins valuations. The argument, essentially, is that the broadly diversified and shareholder-friendly US market will likely continue trading at a premium

to most other equity markets where the hopes of investors are tied year-in and year-out to the fates of a few companies or sectors. This confidence in the future of US equities is bolstered by the fact that new companies and industries are continually being created and taking the place of older companies and dying industries.

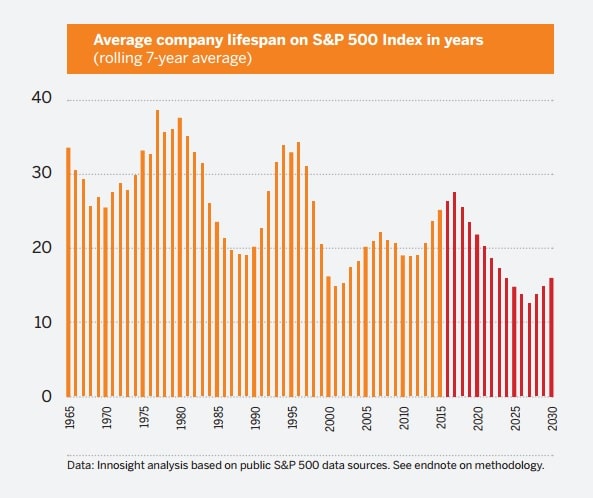

In recent decades, however, this dynamism – as evidenced by the churn in the bellwether S&P 500 index – has become turbocharged. According to a recent study by research firm Innosight, roughly half of the S&P 500 components are likely to be replaced over the coming decade. To illustrate better this point, it is helpful once more to revisit Innosight’s great visual:

While this dynamism certainly shows the health of the US economy and markets, and, in my opinion, explains much of the valuation differences between US and foreign equities, there may also be a downside to it of which not many investors are aware.

To explain why, allow me to take a step backward. If we were to take a step back in time to the beginning of the 20th century and create an index fund, chances are it would be very top-heavy in railroads, as, according to Credit Suisse, they made up more than three-fifths of the US equity market in 1900:

Now, in 1900, railroads were not new technology, having gone through several booms and busts in the 19th century. Yet within the next few decades, the new industries ushered in by the advent of the automobile and the airplane displaced railroads as the chief movers of Americans and their materials. Market indexers would have

This is because a growing number of investors are opting for low-cost index funds (such as those that seek to replicate the performance of the S&P 500), basically opting to buy cheap funds over seeking out cheap stocks, as Dr. Ed Yardeni put it. This is understandable behavior, given the miserable track record of more expensive and far less tax-efficient “active” funds in beating the S&P 500 index.

Now, to be clear, I happen to think that indexing is probably the default choice for most investors, not because I think it is a great portfolio strategy, but mostly because it is convenient, cheap, and superior to the alternatives available to most investors, such as those whose sole equity investments are in deferred compensation plans with limited investment options.

That being said, however, the rate at which the S&P 500 is turning over its components should give investors pause. Because of the nature of how the index is constituted, – weighting its components by market capitalization, – there can be a tendency for the index to over-value certain sectors at the wrong times, such as technology stocks in the late 1990s, or financial stocks in the middle 2000s.