Share repurchases have been somewhat of a controversial topic in the United States of late, with some commentators decrying the use of low interest rates by corporations to lever up and repurchase shares. This practice of buying back stock has been derided as “financial engineering,” presumably because it serves the interests of shareholders over employees who might otherwise enjoy wage increases, or society as a whole, which might benefit from corporate spending on such things as research and development. Controversies over the practice aside, one thing is clear: the practice of buying back shares has grown in prevalence globally, and it appears that the companies that engage in share repurchases have fared better than the overall markets, both domestically, and abroad.

For example, in the United States, the S&P 500 Buyback Index (total return) has pummeled the overall market, averaging annual returns of 13.98% since January of 1994 (the earliest for which I could obtain data), versus 9.05% for the S&P 500 (total return) over the same period (through November):

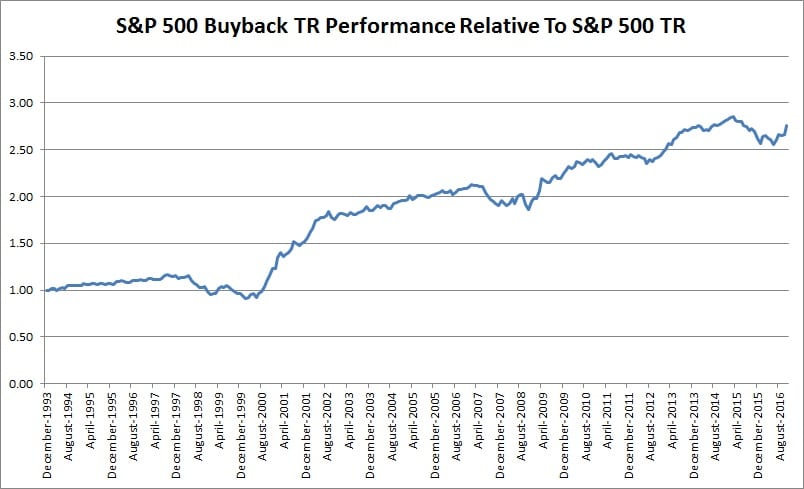

Source: Morningstar

Interestingly, while the two indices tracked each other fairly closely through the 1990s, the buyback index surged ahead after the collapse of the tech bubble in early 2000:

It should be noted, however, that there are likely other factors in play as far as the excess performance of the S&P Buyback Index is concerned. For one, the buyback index is a portfolio of roughly 100 companies that are equally-weighted, whereas the S&P 500 itself is weighted by market capitalization, giving the top holdings a much greater impact on the overall performance of the index. This matters because, historically, equal-weighted portfolios have been shown to outperform portfolios built on market capitalization. Secondly, the buyback index seems focused on higher-quality companies with a value tilt, which historically have outperformed. Consider the differences in valuation between the components of the Buyback Index relative to the mother index. By every measure, the buyback index constituents appear to be much cheaper than the broader index:

The overall outperformance of buybacks has been demonstrated globally, as well. For example, the MSCI Europe Buyback Yield Index has more than doubled the annual return of the MSCI Europe Index since June of 1999, returning 8.09% through November, versus 3.67%:

Source: Morningstar

Similar to the experience in the United States, the parent index fared better through the end of the tech bubble, after which the buyback yield index has surged far ahead:

Of course, just as with its American counterpart, there are likely other factors involved in the dramatic outperformance of the European buyback index. For example, just like the S&P Buyback Index, the MSCI Europe Buyback Yield Index is a more focused portfolio, with only 70 holdings, versus 446 for the MSCI Europe Index. However, the companies are not equally-weighted; instead, the portfolio is weighted by a combination of market capitalization and “buyback yield score.” But the buyback yield portfolio does seem to focus on value-oriented companies, at least on a price-to-earnings basis:

Finally, it should be noted, however, that there are significant differences between the United States and the rest of the world when it comes to repurchases. In the United States, all that is required for a company to buy back shares is board approval, and the managers have wide discretion as far as the timing and pricing of the buybacks. This is in stark contrast to the rest of the developed world markets, where shareholder approval is required, and where managers do not have a lot of flexibility in executing the buybacks.

While share repurchases are gaining in popularity around the world, they are still most prevalent in Anglo-Saxon countries, where shareholders hold primacy over other stakeholders. However, buybacks have only recently become legal in many developed markets; Japan legalized them in 1994, and Germany only in 1998. That, along with cultural issues and the technical factors outlined above, partly explain why buyback yields are still anemic in those countries. Credit Suisse observed that buyback yields are only .7% in Japan, and a meager .3% in Germany. Given the demonstrated superior performance of companies that engage in buybacks, it seems that the trend will continue to favor them going forward.

For further reading:

Credit Suisse: Capital Allocation Outside the U.S.

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.