The recently signed Bipartisan Budget Act of 2015 will have a negative impact on millions of Americans who, as part of their retirement planning would have benefited from “File and Suspend” and “Restricted Application” strategies for taking Social Security benefits. Contrary to the Washington, DC politicians who claimed these strategies were being utilized (hence, in DC opinion – abused) by only the wealthiest of Americans, the reality is much different for millions of middle-class recipients.

It is accurate that 46% of the additional benefits were paid to households residing in the top two income quintiles (40%). On the other hand, 54% of these additional benefits from the File & Suspend and Restricted Application strategies were being paid to the lower 60% of income level recipients (middle and lower income levels).

So, more middle (and lower) income households were utilizing these perfectly legal strategies to provide their families a better financial retirement. Given the above slight tilt towards the “wealthy,” some government officials began to call the Restricted Application and File-and-Suspend rules a form of Social Security “loophole”, and, in 2014, President Obama’s 2015 budget proposal called for changing the rules for these Social Security claiming strategies.

President Obama even stated in his FY2015 budget proposal, that these claiming strategies “allow upper-income beneficiaries to manipulate the timing of collection of Social Security benefits in order to maximize delayed retirement credits.”

So what does all this mean for you? Well, to begin with, if you are already receiving Social Security benefits – these recent changes have no impact on you.

However, if you are within six months of full retirement age, you need to review your options closely. Failure to do so could cost you and your spouse thousands of dollars in Social Security benefits during your retirement years. The changes will take effect after April 29, 2016.

File-and-Suspend along with a Restricted Application for Spousal Benefits allowed members of a couple age 66 or older to delay claiming Social Security based on their own earnings record (so their benefits would increase), while allowing a spouse to receive spousal benefits based on the other member’s earnings record. In addition, a worker who is younger than age 62 at the end of 2015 will lose the ability in the future to file a Restricted Application to claim only a spousal benefit, and then switch to his or her own benefit at a later date (when this benefit exceeds the spousal benefit).

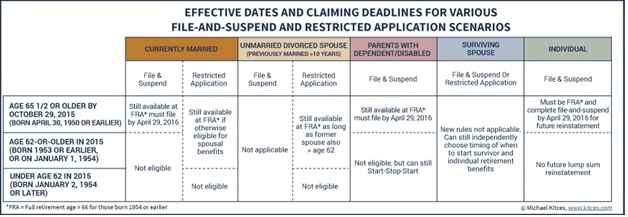

The chart below, courtesy of Michael Kitces of Pinnacle Advisory Group, Inc. in Columbia, MD (kitces.com) provides a table of the effective dates and claiming deadlines for File-and-Suspend and Restricted Application scenarios.

For couples no longer able to utilize the File-and-Suspend or Restricted Application strategies, when to claim Social Security is probably less complicated. However, since the benefits will be less profitable, it’s absolutely critical for a couple to use a synchronized strategy in order to maximize combined benefits.

The following is a summary of new claiming guidelines for two types of couples:

One Earner or One Primary Earner Couples

For couples where only one spouse has qualified for earned Social Security benefits or one spouse’s benefit is more than twice the other spouse’s, it is often better for the higher earner to wait to claim until the lower earner reaches full retirement age. Why? Because spousal benefits stop increasing at full retirement age, so the spousal benefit will remain the same after this point.

One BIG caveat under the new rules is a spousal benefit cannot be received unless the other spouse is receiving a Social Security benefit. So this will add a layer of strategy for the couple before deciding when each spouse should file. As a new rule of thumb, if the higher earner is four (4) or more years older than his/her spouse, the higher earner should file for benefits beginning at age 70 and receive the maximum benefit. The lower earner should claim their own benefit early at age 62, and then pick up the spousal supplement when the higher earner starts collecting benefits.

If both spouses have work history and the lower earner’s projected Social Security benefits are 50% or more of the higher earner, then as a general rule each spouse will receive higher benefits under their own earnings. This is because a spousal benefit is typically capped at 50% of what the other spouse is entitled to at full retirement age.

For a high-earning couple who are the same age, in order for the couple to receive more in benefits if the higher-earner delays benefits until age 70, one spouse must live to at least age 83. The latest longevity statistics show that if a couple reaches age 65, the probability of one member reaching age 90 is approximately 60%. Therefore, this strategy would be the better option.

As in any analysis of when to claim Social Security benefits, there are many variables to consider in your decision. Variables such as current health issues, family longevity history, outside assets available to fund retirement, marital status, income level, and tax bracket (to name a few) are critical to your analysis.

We encourage you to utilize online websites that provide Social Security claiming strategies advice or reach out to us to help determine your best options.