Larry Swedroe had a couple posts (see here & here) this week on emerging markets, and why they are important components of well-diversified portfolios. The main points that Mr. Swedroe makes is that investors should not give up on emerging market equities because they – despite awful recent performance – have performed well historically, and because they are considerably cheaper than US equities.

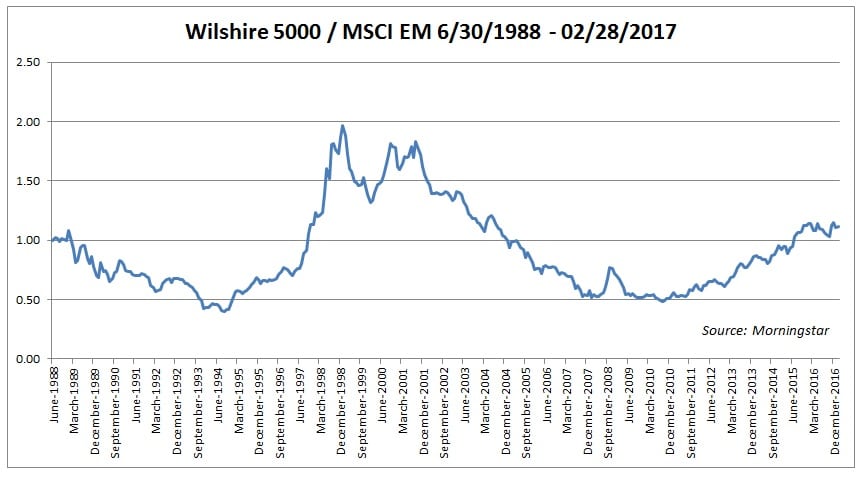

Mr. Swedroe’s point about strong historical emerging market returns is a valid one, but they have tended to generate those returns through long cycles of dramatic over- and underperformance. For example, since June of 1988, the Wilshire 5000 has averaged 10.19% annually while the MSCI EM index has averaged 9.78%, but the paths to those returns were quite different (total return basis in USD):

The cyclicality of the relative returns is immediately apparent, but it is even more telling when compared to the relative performance of other developed markets, such as Europe:

A main reason for the dramatic difference in relative returns is that most emerging market indices and funds are not very well diversified. For example, looking at the major sector representation within the MSCI Emerging Market Index – a widely-referred to index for EM investing – reveals that the index, which is weighted by market capitalization, has far less exposure to “defensive” or acyclical industries such as healthcare and consumer staples than the developed markets in the US or Europe:

Thus composed, emerging market portfolios are obviously going to track more closely the cyclical fortunes of the global economy, particularly the demand for energy and other natural resources. It is little surprise, then, that the volatility of the EM portfolio, as measured by standard deviation, would be roughly 1.5x that of the Wilshire 5000, and 1.3x that of the Europe index.

In light of this cyclicality, it is helpful now to consider Mr. Swedroe’s points regarding relative EM valuations. Mr. Swedroe writes:

“The best predictors we have of future returns are current valuations. With that in mind, the table below provides the valuation metrics of Vanguard’s 500 Index Investor (VFINX) and its Emerging Markets Index Fund (VEIEX). Data is from Morningstar as of Jan. 31, 2017.

As you can see, regardless of which value metric we look at, U.S. valuations are now much higher than emerging market valuations. Now, it’s important to understand that doesn’t make international investments a better choice. Their higher valuations simply reflect the fact that investors view the U.S. as a safer place to invest. And as you know, there’s an inverse relationship between risk and expected returns (at least there should be).”

Mr. Swedroe is quite correct to point out the valuation gap between US and EM equities, but given what we have outlined above, the discount on EM equities should not be surprising. As mentioned previously, they are less diversified across major sectors and their cycles tend to be more exaggerated (i.e., they are more volatile). In addition, the majority of EM portfolios, as we discussed in a previous post, tend to be composed of equities from countries such as China and Brazil that have histories of political unrest, inflation, and other hazards that are somewhat foreign to the American or modern European imagination.

Tellingly, a penetration of the fund or index wrapper reveals that the biggest valuation disparities between US and EM stocks can be found when comparing sector valuations:

US vs EM Trailing Twelve Months’ Price-to-Earnings (or “P/E), and Price-to-Book:

US vs EM Price-to-Sales and Price-to-Cash Flow:

Generally speaking, across the various measures of valuation, the sectors in which the US trades at substantial premiums are the sectors such as energy, financials, and utilities. As WisomTree’s Jeremy Schwartz has written, these sectors are deemed “public goods,” and thus have far more government ownership (generally through “SOEs,” or state-owned enterprises) and involvement than other industries such as consumer staples. Likely for this reason, the valuations of emerging market sectors less exposed to government ownership or interference currently have valuations more closely in-line with US and other global market valuations.

A good example of this disparity between the valuations of an American energy company and an EM energy SOE are Chevron and Brazil’s Petro Brasileiro:

Both companies are in the oil business, producing and marketing a product that is essentially fungible, meaning that there is no real difference between their products. Yet the American company, Chevron, trades at a substantial premium because investors in the company are more focused on the business of energy production, and are not overly burdened by the extracurricular concerns involved with doing business with an EM SOE, such as possible corruption, property rights, and other variables that come into play when an EM government is your business partner.

Conversely, we can examine the valuation differences of two beer producers, Brazil’s Ambev, and Molson Coors:

The valuations of the two brewers are much more similar than the two energy giants, and in fact the Brazilian Ambev trades at a premium across the board. This is noteworthy because both Petro Brasileiro and Ambev, being Brazilian companies, are subject to the same macro headwinds that all investors in Brazil face, yet despite this, one company still commands a premium valuation to its American peer, while the energy SOE trades at a steep discount. This further supports the claim that a great deal of EM “cheapness” resides in a few sectors, and for good reason.

What Should EM Equity Investors Do?

These concerns should not drive investors away from investing in emerging markets. After all, as Burton Malkiel has written, emerging market equities compose almost one-fourth of global equity market capitalization, which is simply too large a segment of the global equity pie to ignore:

(from Burton Malkiel / Wealthfront)

The most popular – and cheapest – ways to access emerging markets are through ETFs such as those iShares and Vanguard offer. The trouble with these funds, however, is that they are market-capitalization weighted, meaning that they will give investors heavier exposure to countries such as China, and sectors such as materials, that are heavily dominated by SOEs. This means that most of the popular EM indices and the funds that track them are less balanced and more volatile than strategies that offer more equal representation for the smaller and more acyclical sectors in emerging markets.

This may mean that your overall portfolio will have more exposure to cyclical industries than you intend, and that you are effectively adding more volatility to your portfolio even though you are saving on fees. This is likely a poor recipe for successful EM investing, given the elevated volatility of emerging market equities, and that investor tendency is to sell at inopportune times.

One would think that less efficient markets would mean that active EM management would produce better-constructed portfolios with superior results, yet this hasn’t been the case. As Mr. Malkiel observed in the same article referenced above, actively-managed EM funds have fared no better than their peers in the US and elsewhere:

(from Burton Malkiel / Wealthfront)

One possible strategy would be to employ an equal-weighted strategy by sector. MSCI has just such an index, with data going back to the beginning of 1999. This strategy yielded superior results over this time frame ending in February 2017, with the sector equal-weighted index yielding annualized returns of 10.6% versus the market-cap index’s returns of 9.3%. Furthermore, the sector equal-weighted index did so with less volatility, and a shallower maximum drawdown, -55% vs -61%:

Given that this strategy has historically yielded superior results when modeled with US equities, it would seem a perfect fit for emerging markets, given that it would reduce cyclical industry exposure, and tilt EM portfolios away from heavier weights in SOEs. Unfortunately, however, there appear to be no low-cost funds or ETFs that employ this strategy, and there are few if any EM sector ETFs that would make replicating such a strategy feasible and cost-effective.

One fee-efficient and tax-efficient way to implement a more sector-balanced strategy might be to complement your EM index fund or ETF with an instrument such as the iShares Minimum Volatility EM ETF, symbol EEMV. Relative to the market-capitalization weighted EM ETF, EEMV offers investors more exposure to consumer staples and healthcare, and less to materials and energy:

Besides the advantage of more balanced sector representation, such a strategy does not necessarily mean that an investor would be sacrificing the relative valuation advantage of emerging markets; in fact, per the iShares website, EEMV’s weighted price-to-earnings ratio (based on the last twelve months’ earnings) is about 16, versus 13.6 for IEMG. Similarly, EEMV’s weighted price-to-book ratio is 2.17, which is above IEMG’s 1.5, but well below the 2.96 of the MSCI USA Index.

In sum, indexing using generic, low-cost ETFs and funds is probably adequate for many, if not most, investors. However, given the unique characteristics of emerging market equities, there are ways to add more balance to the EM portion of a portfolio without sacrificing much of the benefits of low-cost index investing. As the trend toward indexing continues, hopefully that will mean more low-cost EM funds of superior composition than simply market capitalization.

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Clients of Fortune Financial own shares of EEMV, TAP, ABEV, and CVX.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.