There’s a lot of chatter today about the major decline in publicly traded firms (h/t Ritholtz Wealth’s Josh Brown). This is not a revelation; industry commentators have been discussing the phenomenon for several years now. I am sure there are several explanations for this: the financial crisis forcing many banks to merge or go under; the tech bubble’s bursting laying waste to many firms that IPO’ed prematurely, etc. However, determining the causes of the change in the capital cycle is not the point of this post. Rather, I am going to show which industries have added and subtracted the most companies over the last few decades just to give some perspective to what has transpired in the public markets.

First of all, I used Professor Ken French’s wonderful data library (specifically the 49 Industry Portfolio data set) to run the numbers. Here are the caveats:

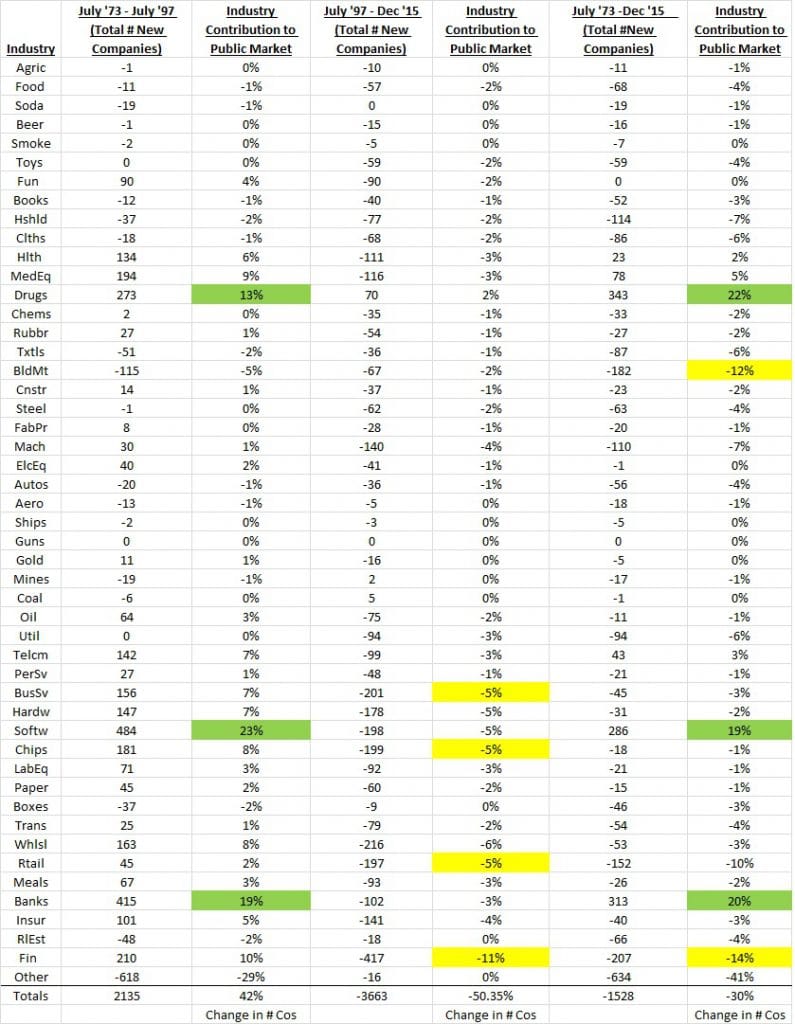

-Because there is an explicable jump in the total number of companies between June and July 1973, I decided to start with July 1973 in an attempt to smooth out possible anomalies.

-You will see that the largest category in the industry column is “other;” this is Professor French’s designation. While I cannot speak for his reasoning for categorizing companies as such, I can only imagine he didn’t think they contributed overall to any of the other 48 industries listed. That being said, I more or less chose to ignore that category.

Here are the results:

You can see that during the market’s expansion phase from July 1973 to July 1997 (the peak for total number of listed companies in the data set), drugs, software, and banks accounted for the bulk of new company issues. Conversely, during the contraction from July 1997 to the end of 2015, banks, chips, and business services have led the way.

Amazingly, there are some 30% fewer public companies now than even in July 1973. Obviously, some industries such as software and banks have welcomed many new public participants, while a few such as miscellaneous financials and building materials have been shrinking all along.

As a clarification, I decided to present the “% decrease/increase” columns as negatives; i.e. from July 1997 till December 2015, Financials declined 11%. I show it as -11% to show that it was responsible for 11% of the market’s overall contraction.

Appendix – expanded table to include % change in industries during each time-frame: