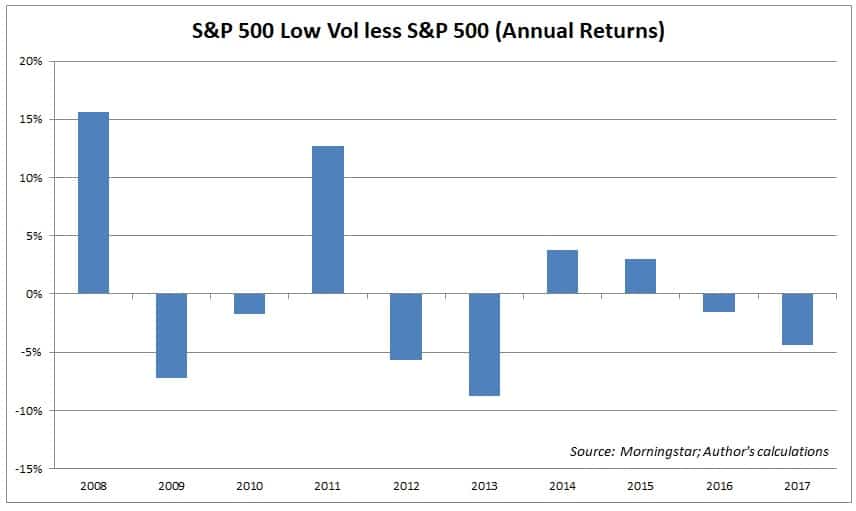

2017’s strong market resulted in the largest outperformance for the S&P 500 index versus its low-volatility counterpart since 2013:

In fact, last year saw the S&P 500 low-volatility index fail to outperform all but a handful of the other factor benchmarks, trailing the growth and momentum indices by more than 10% each (via SPIndices):

Largely as a result of this relatively poor performance, assets have been bleeding from the popular ETFs that track the S&P 500 and MSCI low-volatility indices. With the market off to another strong start in 2018, it would not be surprising to see even more investors exiting low-volatility strategies.

However, as a long-time proponent of low-volatility investing, I would not encourage you to follow suit. There are many advantages to low-volatility strategies such as the consistency of their returns, about which I wrote last summer. Additionally, low-volatility strategies have generally suffered shallower drawdowns with shorter durations than the broader market:

Furthermore, while investors may be inclined to think that risk necessarily equals more reward, the opposite is true in this case; since November of 1990 (the earliest point for common data), the S&P 500 Low-Volatility Index has outperformed the S&P 500 Index by 80 basis points annually, with 70% upside capture, but only 50% of the downside capture:

Importantly, since 1995, low-volatility has more or less performed in-line with last year’s best performer, momentum, with quite favorable risk-reward characteristics:

In light of these comparisons, investors would be wise to reconsider abandoning low-volatility strategies, especially now that the market is, by almost any measure, expensive, and volatility has been uncharacteristically benign for so long. Low-volatility investing should continue to be a good way to maintain exposure in an expensive market while being positioned advantageously for the inevitable correction.

NOTE: For anyone interested in investing in low-volatility strategies, it is important to understand that there are vast differences between some of the more popular low-volatility indices and the ETFs that track them. For example, relative to the broader market, the MSCI low-volatility ETF (symbol USMV) deviates less from the S&P 500 sector composition (as measured by the SPDR ETF, SPY) than does the S&P 500 low-volatility ETF (symbol SPLV), as can be seen in the graphic below (data as of January 2018):

Clients of Fortune Financial Advisors, LLC own USMV.