Charlie Bilello of Pension Partners has an interesting piece titled “The Volatility Cycle” in which he lays out the history of the S&P High Beta and S&P Low Vol indices going back to their common inception in November of 1990. He notes that, because of recent outperformance by low-volatility sectors such as consumer staples and utilities, the Powershares Low Vol ETF (SPLV) has taken in almost $7 billion in assets while its high-beta counterpart, the Powershares High Beta ETF (SPHB), has taken in only about $88 million in new assets (since 2011).

Given that SPLV’s performance (13.05%/yr from Nov. 2011 through April 2016) has dwarfed SPHB’s (5.96%/yr over the same period), Mr. Bilello wonders whether the massive inflows into low-volatility themed investments are simply chasing performance, and, what’s more, possibly overpaying for past performance.

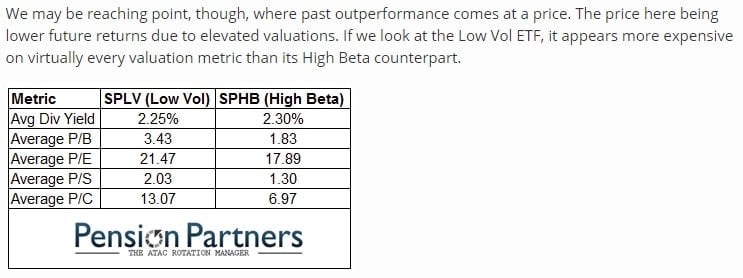

Writers Mr. Bilello:

By those metrics, the high beta portfolio is cheaper, and significantly so.

Certainly, Mr. Bilello isn’t the only one to wonder about inflated valuations and performance chasing in low-volatility funds. Josh Brown of Ritholtz Wealth wrote on his site that investors have been pouring money into the iShares low-vol ETF, USMV:

[Note: all data from Morningstar unless otherwise indicated.]

Like SPLV, the internals reveal that USMV seems perilously expensive:

It might be tempting to extrapolate from the valuations of, and the inflows into, these low-vol ETFs that there is a kind of bubble in low-vol stocks and sectors of all kinds. I think that is a mistake, and an alternative assessment of these portfolios seems to confirm that.

First of all, comparing the sector composition of SPLV and SPHB reveal obvious differences. You can see from this table that the low-vol portfolio has no exposure to technology and energy, and it’s heavily weighted in staples and utilities:

Conversely, the high-beta portfolio has no exposure to staples and utilities, and is heavily weighted in energy:

Given that SPLV has only 102 total holdings while SPHB has only 98, I wondered whether these are fair representations of their respective factors.

To test that, I used the same weightings above, and I allocated accordingly to the various sector ETFs (such as XLP for consumer staples, for example). What I discovered is that the “low-vol remake,” as I called the alternative low-vol portfolio, had much lower valuation metrics than SPLV:

Only on a P/E basis is this alternative low-vol portfolio more expensive than its benchmark, the S&P 500. [Incidentally, while the 3-year standard deviation is only slightly higher (10.24 vs 10.18 for SPLV), the Sharpe ratio for the alternate low-vol portfolio is considerably higher at 1.13 vs .99.]

Performing the same analysis on USMV reveals much the same thing:

Here is the sector breakdown for USMV:

And here are the valuation metrics for the similarly-weighted alternative low-vol portfolio:

Clearly, it’s quite a bit cheaper than USMV (see above), and it’s is cheaper than the S&P 500 on a Price-to-sales and price-to-cash-flow basis.

Now that I’ve made the case that just because low vol ETFs are expensive doesn’t mean that low-vol portfolios are, I think it would be instructive to see whether high-beta portfolios are as “cheap” as they appear. Here are the results for the alternative high-beta portfolio:

You can see from comparing these numbers with Mr. Bilello’s table above that just because the high-beta ETF looks compellingly cheap, similar “high beta” portfolios may not be.

The point of this exercise was to caution investors against extrapolating too much from the unique characteristics of factor ETFs that designed to replicate unique indices. Also, each fund manager who builds a factor-themed portfolio may have different criteria for doing so, and thus valuations and so forth can be very different from one fund to another even though the aim of the fund is to provide exposure to the same factor. Furthermore, while using sector ETFs as proxies for building alternative low-vol and high-beta portfolio may not be perfect, the fact that these portfolios include many more stocks than funds like the Powershares ETFs leads me to believe that perhaps they offer a more complete picture of exactly what is going on in the marketplace valuation-wise.

Note: if you are interested, the specific sector ETFs I used in these models are these: