In his latest quarterly letter, GMO’s always interesting Jeremy Grantham lamented the refusal of U.S. equity valuations, and the stubbornly high profit margins that have sustained them, to revert to the long-term average. Grantham writes:

“We value investors have bored momentum investors for decades by trotting out the axiom that the four most dangerous words are, “This time is different.” For 2017 I would like, however, to add to this warning: Conversely, it can be very dangerous indeed to assume that things are never different.”

This seems to me to be a prudent caveat; after all, the period for which we have reliable equity data is trivial in the scope of recorded human history, and the markets for which unbroken data are available are very few. Therefore, assuming all future cycles should revert to the recorded mean observed over a couple hundred years is imprudent; assuming they will revert to the recorded mean observed over the few decades with reliable data may very well be folly.

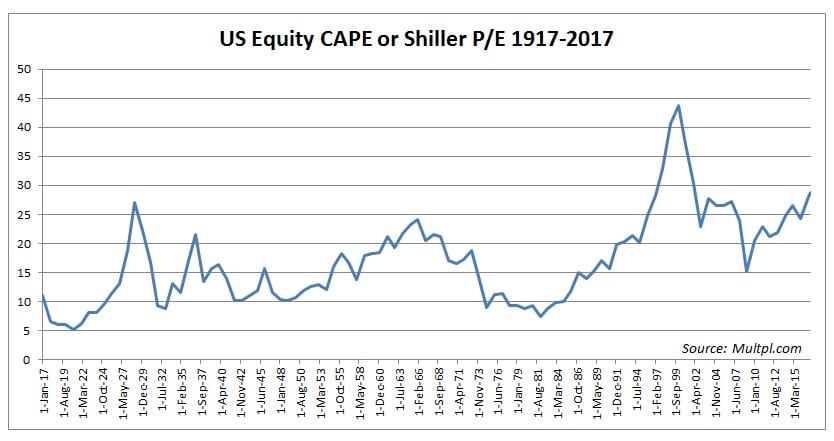

Furthermore, the main problem with basing investment decisions on mean reversion is that it ignores what causes the mean reversion in the first place. Consider the widely-cited Shiller P/E ratio, which is, as is widely discussed, well-above it’s long-term mean:

In 1975, the series, which from 1881 through 1974 averaged about ~15, touched single digits for the first time since the Depression. The series would not regain its average of ~15 until 14 years later. Would the ratio have dropped below the historic mean to single digits in the 1970s absent double-digit inflation and the poor policy choices that spurred and prolonged it? Would the series have regained its average absent better policy choices that tamed inflation and restored confidence in long-term investments?

Obviously, none of the external factors that served to compress or elevate equity valuations were preordained. The only usefulness in the observed average, then, was for willing investors to make a bet that, in the first case, things had become too euphoric and were due to cool off; and, in the second place, that competent policymakers would eventually figure things out. In other words, the data provided a reasonable margin of safety to make an educated bet that by no means was guaranteed.

Fast-forward to the present day where you have the U.S. market trading at a historically rich CAPE ratio of about 29, and, on the other end of the spectrum, Russia trading in the low single-digits. Relying on mean reversion alone would dictate a rotation out of expensive U.S. equities and into Russian equities, the assumption, apparently, being that profits in the U.S. were overdue for a fall, and that pessimism on Russian equities was overdone. Logically, of course, this makes sense. Value investing, after all, is really two-pronged: buying cheap assets while at the same time avoiding expensive ones. Yet fundamentally this double bet on mean reversion is misguided; there is nothing to say that Russian stocks cannot fall further in valuation, – after all, they have been wiped out before by political revolution, – and there is no reason to believe, especially in an era that has seen negative interest rates for bonds maturing in a decade, – an actual guaranteed loss of money over ten years!, – that valuations in the U.S. cannot rise further. All it really tells us is that the earnings on Russian stocks yield more than in the U.S., and that they should return more going forward, all else being equal. It is far from guaranteeing it.

This is not meant to be another defense of rich stock valuations, and an argument that this time, unlike period of rich valuations in the past, actually is different. Rather it is meant to be a clarification of where we stand. In 1929, while much of Europe was still laboring to recover from a devastating war that depleted its capital, maimed its manhood, and crushed its spirit, the U.S. was enjoying a long and uninterrupted period of prosperity that had seen isolated farmers liberated from the monopolies of local merchants by the automobile, and most householders in major cities enjoying the wonders of electric lighting and indoor plumbing*. In 2000, the world was thought to be entering a new period of prolonged peace and interconnectedness with the computer and the internet as its vanguards. In each case, new industries and companies went public at a rapid pace; valuations on companies with little or no profits skyrocketed. As Howard Marks wrote in January of 2000, what linked 1929 and 2000 was the euphoria that surrounded new ideas and industries, and a fundamental overestimation of the profitability of their life-changing capacities.

The U.S. market today, even though nominally valued similar to those notorious bubble peaks, is behaving with less euphoria than what characterized it in 1929 and 2000. Mergers of existing players have continued unabated, and IPOs are well below the pace of the last few decades. Indeed, it is as though the U.S. market as a whole has undergone what has happened to many industries previously, and that is that it has matured. Profit margins and valuations are likely where they are precisely because the weak hands have been culled from the herd, whether by the equity debacle in the wake of the tech bubble, or the bankruptcies that resulted from the worst economic downturn since the Great Depression. In fact, the U.S. equity market seems to be in a kind of sweet-spot by which I mean it is diverse and liquid enough to enjoy a competitive advantage over almost all other global equity markets yet, at the same time, the pace of creative destruction has slowed sufficiently for industries to concentrate and for profits to remain elevated as a result.

Perhaps it is this balance that explains if not justifies rich valuations, but it should serve at least to frame them in a way that makes them understandable. The problem with rich valuations, it goes without saying, is what, if anything, to do about them. There are certain laws of mathematics that would seem to dictate that U.S. equities, with a current CAPE earnings yield (the inverse of the CAPE ratio) of about 3.5%, will deliver disappointing results over the subsequent decade simply because valuations can expand only so much before yields approach zero.

Knowing that future returns are, at least, less likely to deliver similar returns to what they have in the past, the dilemma for asset allocators, then, is whether to avoid U.S. equities altogether assuming a reversion that may never happen to a mean that probably no longer applies, or to place increasingly large bets on foreign and emerging markets less richly valued, but also, perhaps, justifiably so. Yet avoiding U.S. stocks altogether while waiting for valuations to mean-revert is as foolish as avoiding bonds while waiting for rates to rise.

Common sense would dictate that behaviors will have to adapt to this new period of low yields that applies to every asset class by reducing expenses, limiting debt obligations, and saving more. It does not mean, in my view, to take drastic action with your portfolio by which I mean exiting U.S. equities altogether, or to perform the equity equivalent of what bond analysts deride as “reaching for yield” by going all-in on seemingly cheap markets such as those in the emerging world. Far more capital has been lost in opportunity cost or speculations than by riding out normal valuation corrections, and investors who attempt to do too much with their portfolios will likely suffer the most. As Jeremy Grantham noted, perhaps a new era has indeed begun, and investors should adapt accordingly.

*Source: The Rise and Fall of American Growth by Robert Gordon.

For further reading, see “Mean Reversion: Gravitational Super Force or Dangerous Delusion?” by Professor Aswath Damodoran

http://aswathdamodaran.blogspot.com/2016/08/mean-reversion-gravitational-super.html

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.