Some time ago, I wrote an article that explored the Dow Jones Industrial Average’s superior performance to the S&P 500 over the last few decades. In broad terms, the Dow’s excess performance has been aided by fewer concentrated sector bets over time, leading to shorter and less pronounced drawdowns after “bubble” periods (think 1999-2000, and 2006-2009). However, the more precise academic explanation is that the Dow has benefited from greater tilts to factors such as quality and value.

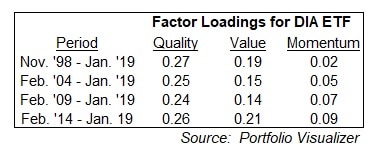

An additional factor that has been persistently positive in the DJIA, – albeit not as strong as value and quality, – has been momentum. Using the SPDR DJIA ETF (symbol DIA) to run factor regressions with Portfolio Visualizer, we can see that since DIA’s launch in late 1998, the Dow has had a very slight positive loading on momentum over the last twenty-plus years, though of course it loaded higher over various increments over the period:

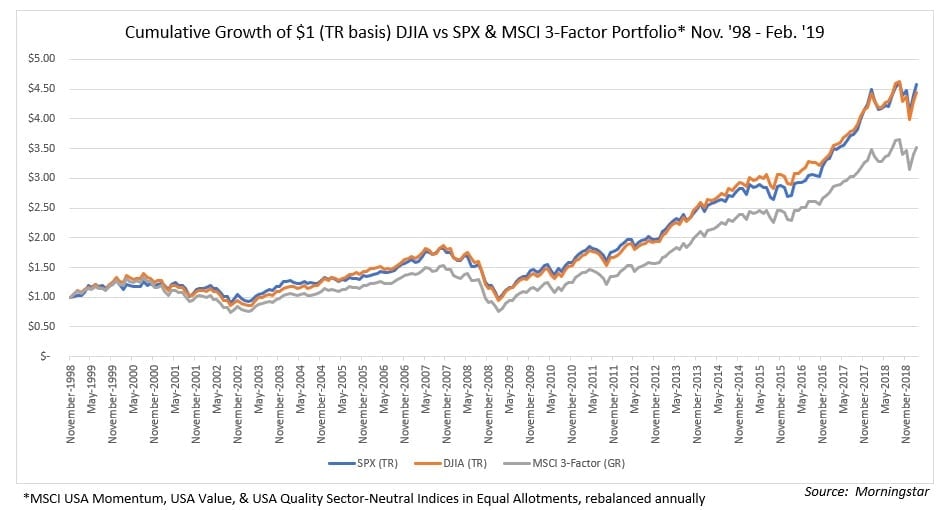

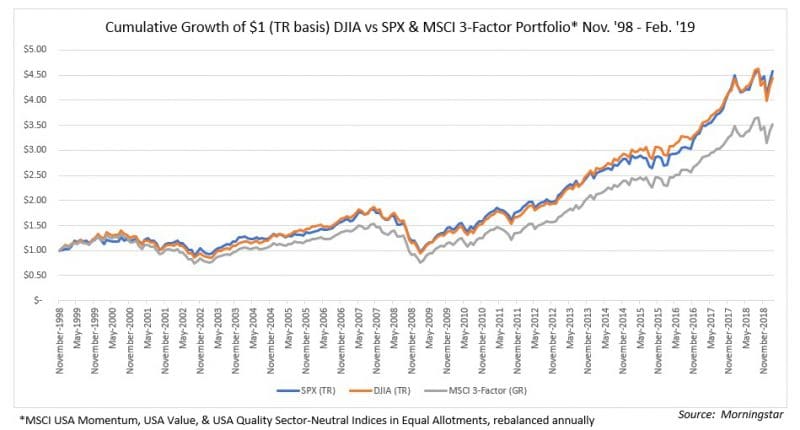

Another interesting way to see effects of the factor loadings in the DJIA is to simulate a proxy factor portfolio of value, momentum, and quality, and compare the results. To run this simulation, I created a “3-Factor” portfolio that is equal parts MSCI USA Momentum, MSCI USA Value, and MSCI USA Quality Sector Neutral, and rebalanced annually [Note: this simulation uses gross returns for the MSCI indices, and total returns for the S&P and DJIA.] One can see that over the last two decades, the simulated portfolio tracks the DJIA pretty closely:

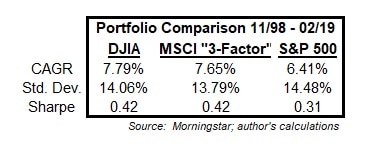

Furthermore, when one looks at portfolio statistics, the similarities between the simulated “3-Factor” portfolio and the DJIA are striking, with the DJIA and the “3-Factor” portfolio registering identical Sharpe ratios:

Certainly, the Dow has its critics as far as being a barometer for stock market health; after all, it is fairly concentrated (it is composed of thirty companies), and is price-weighted, which is not really ideal in terms of lining up one’s desired exposure to fundamentals. However, the fact remains that, coincidence or not, the factor exposures have been reasonably consistent over a lengthy period of time, despite numerous additions and substractions to the components over the same period. Whether or not this persists going forward is, of course, anyone’s guess, but a fairly long history of consistent results suggests the DJIA’s utility as a kind of poor man’s multi-factor index should not be discounted.

Disclosure: Clients of Fortune Financial Advisors, LLC are long DIA.