Tadas Viskanta over at Abnormal Returns has an interesting symposium today on the topic of what investments might be better investments over the next decade than the S&P 500. The suggestions made by his featured guests are varied and creative, and they are worth checking out. However, I would like to add a suggestion or two of my own.

My first suggestion is a featured theme of my articles, and that is the consistency of seeming timelessness of tobacco stocks. Last year, I covered this topic in great depth, so there’s no need to repeat it again here. For those interested, my article on selecting Altria as one stock for the next twenty years can be found here.

My second suggestion is similar in that it follows a kind of defensive theme. One key attribute of a successful investment is obviously not just its potential to outperform, but also the likelihood of an investor to realize that outperformance. My theory here is that an investor is less likely to sell a good investment if its returns are consistent and not overly volatile, so this factored into my thinking. Secondly, in an era where just about every segment of the global equity market is fairly valued at best, the next ten years bring quite a bit of uncertainty, both for the economy as a whole, and for the market in particular. Therefore, I think a conscious decision to overweight one sector or investment over the broader market should take these factors into account.

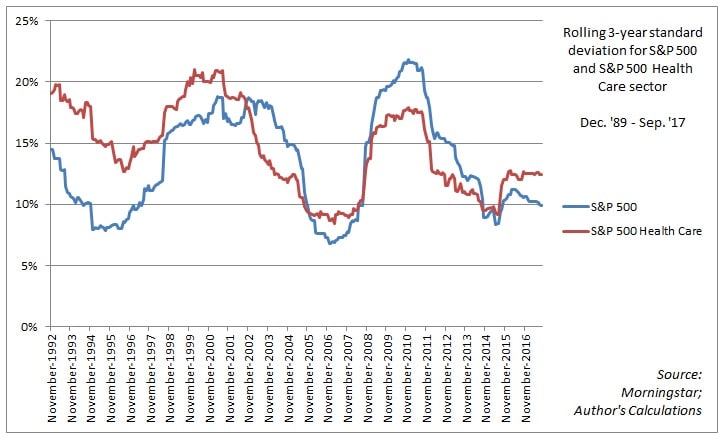

All that being said, I believe the case for health care stocks is pretty strong. For one, since data begin in late 1989, the S&P 500 Health Care sector has handily outperformed the broader S&P 500 index, 11.8% to 9.6%, and it has done so with roughly equal volatility…

…and shallower drawdowns:

Furthermore, as of September 30th, the S&P 500 Health Care sector traded at slight discounts to its twenty-year history when considering both trailing and forward-looking price-to-earnings multiples. This stands in contrast to the broader S&P 500 index, which currently trades at a premium to its twenty-year history according to both valuation metrics:

It would seem that valuations, then, are currently favorable, however slightly, and I have already demonstrated that health care stocks have, historically, enjoyed a favorable risk profile compared to the broader market. That leaves the question of how health care stocks will perform over a long period (again, ten years) of possible economic uncertainty.

I would venture to guess that health care stocks stand a reasonable chance of maintaining their edge when it comes to a favorable risk profile. Consider this chart from Chris Pavese, which shows that profit margins for health care stocks have been remarkably stable over the last twenty years, a period which encompasses two recessions, one of which was very severe:

Secondly, a study of previous recessions by McKinsey & Company showed that, along with consumer staples and utilities, the health care sector has generally suffered much shallower declines in earnings during recessions. For example, consumer spending on health care was the one area of household expenditures that saw an increase in the years 2007-2010, the period generally associated with the Great Financial Crisis. It seems unlikely that this trend will change as demographics ensure an ageing population with a necessarily higher rate of spending on health care.

If one is so inclined, a superior way to make a long-term bet on health care stocks would be to equal-weight the portfolio. Since the start of 1990, the S&P 500 equal-weighted health care sector (14.3% CAGR) has outperformed both the broader index and the market capitalization-weighted S&P 500 health care sector, while suffering less severe drawdowns:

Similarly, perhaps due to the rebalancing implicit in equal-weighting, which results in tilts toward value and small companies, the equal-weighted health care portfolio has delivered positive returns more consistently than both the cap-weighted sector index and the broader S&P:

In sum, given slightly favorable valuations and what historically have been favorable risk-reward characteristics, a long-term bet on health care stocks seems as sound a bet as any. There are, to be sure, potential headwinds such as political risk, especially when health care reform has been the topic of years of political debate. However, there are idiosyncratic risks associated with overweighting any sector or investment over the broader market, and those associated with health care seem no more dire than those affecting other sectors of the market.