“The facts are overwhelming. Stocks of spinoff companies, and even shares of the parent companies that do the spinning off, significantly and consistently outperform the market averages.” – from You Too Can Be a Stock Market Genius by Joel Greenblatt

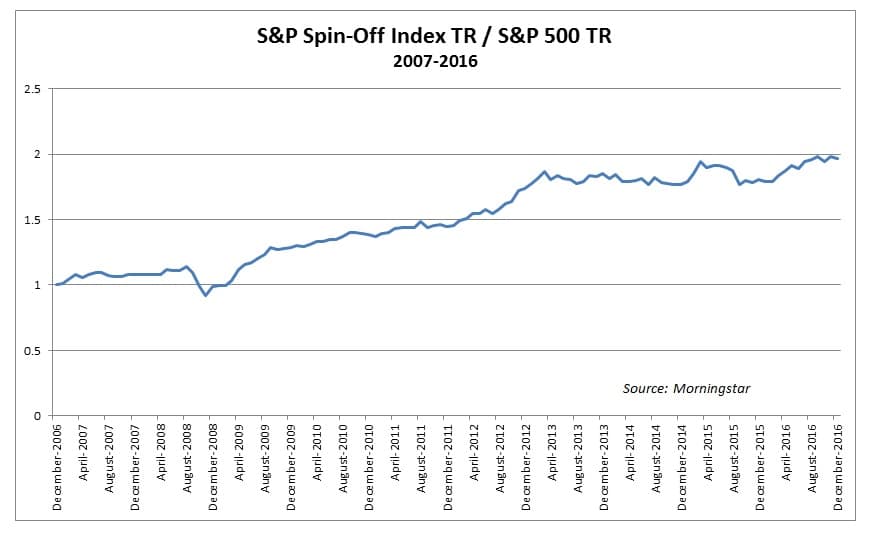

Though it was twenty years ago when Mr. Greenblatt wrote about stock spinoffs in his classic investment treatise, the wisdom of his observation is still valid. In fact, an investor would have done well had he heeded Mr. Greenblatt’s advice; the S&P 500 Spin-Off Index, since its inception in late 2006 through the end of 2016, has handily outperformed the S&P 500 itself, 14.43% vs 6.94%:

To explain this large difference in performance, it would be helpful to explain what exactly stock spinoffs are. In simplest terms, a stock spinoff is a tax-free divestiture of one company by another, which results in the shareholder of the original company now owning shares of both. The net effect is that the separate companies are now freed up to focus on their respective core businesses.

According to Deloitte’s study of spinoff performance, this dynamic is likely the main reason for the success of spinoffs. As the authors write, conglomerates tend to be undervalued, likely because investors are reluctant to assign premium valuations to many-faceted corporations with fewer synergies than more streamlined and focused businesses. The result of the spinoff is that both the “spinner” and the “spun” companies appear more transparent in their operations and business results, and thus are more attractive to would-be investors.

The idea that streamlining unlocks value for both parties seems to be borne out in the actual returns. As The Economist noted, between 2002 and 2012, there were some 80 spinoff transactions in the United States, with both the divesting and divested companies handsomely beating the broader market averages.

Lest anyone think that spinoff performance is a purely American phenomenon, the returns of foreign spinoffs have been just as stellar as those of their American counterparts:

[It should be noted that the Horizon Kinetics Int’l Spin-Off Index, referenced in the graphic above, is a very narrowly focused index with an average of fewer than thirty components in each of the years shown.]

Investing in spinoffs, however, may not be as simple as the index returns suggest. For one thing, spun-off shares tend to take a tumble in the days and weeks after being spun, which could lead many investors to sell these unfamiliar shares out of their portfolio:

Although investors might think this initial weakness is signaling dire prospects for the new company, the reality is that the weakness in the new shares has little or nothing to do with the fundamentals of the company. Rather, the decline is due to reasons that are mostly technical. Credit Suisse explains that the new shares may not meet the criteria necessary to remain in the index or portfolio that holds the parent company, and so forced selling occurs. Eventually, the forced selling subsides, and the shares recover.

Spinoffs are not without risks, though, and they are by no means universally successful. In truth, some spinoffs can be the result of a parent company wanting to jettison unwanted liabilities or lagging businesses, and for these reasons, spinoffs such as these, which are now cut off from the resources of the larger, perhaps more diversified parent firm, can be especially vulnerable. As always, investors need to take these factors into consideration when entertaining a prospective investment.

The broader lesson, though, is that spinoffs, like stock buybacks, are nothing mysterious or devious, as some in the financial media may want you to believe. They are, simply put, just another way for corporations to unlock value for their shareholders. Corporations that focus on maximizing value for their shareholders – in whatever form it takes – are likely to continue to prove to be the best stewards of your investment capital.

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.