If I were to tabulate the total number of articles sent to me by clients and colleagues about the market and projections for its future, I can safely say that close to 90% of those articles were of the extremely pessimistic variety. This is to be expected; it is well-documented that negative headlines and dire predictions get far more attention than reports of the mundane. If you are in the media business, your job is to entice interest, and, unfortunately, it seems that there is a large market for the consumption of pessimism, no matter how far-fetched the claim, let alone how little the probability of some apocalyptic event occurring.

There is, however, another kind of pessimism: that of the Cassandra. These perpetual pessimists, especially those who are involved in the markets, have cultivated a large following based on having been right once or twice many years ago about a market peak and subsequent crash. In many ways, through their blog posts and articles, they behave like the Old Testament prophets of doom, almost claiming to share their extreme anxieties about the market not as content to be consumed, but as a public service since, I suppose, the majority of us are blissfully ignorant of inevitable market carnage.

John Hussman is one of these people. He is certainly a very bright man, and he provides very good context and data to back up his dire warnings. This is truly commendable as it must be extremely laborious to issue warning after warning:

November 2010: Bubble, Crash, Bubble, Crash, Bubble…

March 2011: Anatomy of a Bubble

March 2012: A False Sense of Security

November 2013: A Textbook Pre-Crash Bubble

July 2014: Yes, This Is An Equity Bubble

October 2015: Not The Time To Be Bubble-Tolerant

October 2016: Sizing Up the Bubble

Since the publication of that November 2010 article, the S&P 500, which Mr. Hussman has repeatedly warned us has been in a bubble, has returned over 100% on a total return basis. It must be exhausting – not to mention humbling – to be so dedicated to an idea that, despite all your evidence to support it, is repeatedly rejected by investors who have continued to bid shares higher and higher.

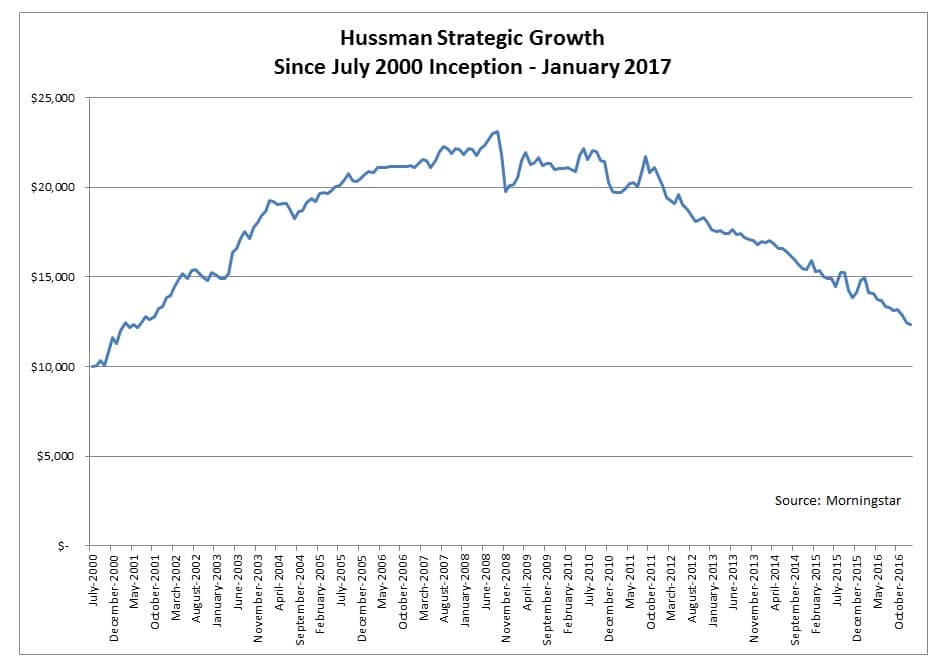

In fact, since the current bull market began in March of 2009, Mr. Hussman has repeatedly called for a titanic decline in the S&P 500, but, in a twist of irony, it has been his own fund, Hussman Strategic Growth (HSGFX), that has suffered a disastrous bear market all its own with a peak-to-trough decline of almost 50%:

While it may be tempting to poke fun at Mr. Hussman, who likely thinks of himself as a “voice crying in the wilderness,” there is a valuable lesson here for investors.

In April 2007, Mr. Hussman mockingly wrote of Jeremy Siegel that the latter’s bullish stock market forecast of real returns of “6.0 to 6.5 per cent on S&P 500 stocks” was absurd, and that Professor Siegel’s bullishness was an example of “hubris” (his word), and that Professor Siegel was in danger of becoming the new Irving Fisher. I cannot speak with certainty as to the criteria for Professor Siegel’s cited forecast, but it is telling that since Mr. Hussman published his criticism of Professor Siegel, the S&P 500 has averaged an annualized real return of about 5.1%. Certainly not 6% or 6.5%, but not far off the mark, either. It goes without saying that it was a far better performance than the average annualized loss of 5.5% suffered by shareholders of Mr. Hussman’s fund over the same period.

Perhaps, if he is honest with himself, Mr. Hussman would admit that it was he and not Professor Siegel who was more hubristic. It is one thing to be dedicated to an idea, but it is quite another to remain attached to it despite all the evidence to the contrary. It is yet another example of how an ideology can corrupt an investment process, and the ones who suffer most are investors whose capital is depleted because a manager is more obsessed with being right than with preserving capital, or, if possible, earning a return on it.

Mr. Hussman’s mania over perceived bubbles has almost a sinister aspect to it. This obsession with prophesying doom no matter what makes Mr. Hussman resemble the naysayer of which Pascal Bruckner has written, “[H]e becomes intoxicated with his own words and claims a legitimacy with no basis…Catastrophe is not [his] fear, but his joy. It is a short distance from lucidity to bitterness, from prediction to anathema.”

Investing is an extremely difficult endeavor, and most will fail at it. All the charts in the world that show stocks have averaged X return over Y period of time are useful only to the extent that investors realize that there were countless periods when stocks lost 10, 20, and even 50% along the way to averaging those returns. While we should heed the counsel of wise men, we should be on guard against the Cassandras like Mr. Hussman, who have wedded themselves to an idea, and who point an accusatory finger at those of us who, having seen the weight of evidence, choose to ignore their warnings. It is to the great misfortune of Mr. Hussman’s shareholders that he has been more preoccupied with being right about the inevitable doom of our investments, at the expense of ignoring the catastrophe suffered by his own.

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.