With interest rates close to all-time lows, and major stock indices hovering just below all-time highs, the hesitancy of many people to invest in either stocks or bonds is easily understood. After all, it seems axiomatic that if stocks are at all-time highs, investing now most likely sets you up as the last sucker to get in just before the bottom falls out. Similarly, if bond prices and interest rates move inversely, buying bonds when rates are depressed means that if rates move up in a sustained fashion, one’s money in bonds will likely take a beating. Faced with those perceived likelihoods, can anyone be blamed for not wanting to invest his or her hard-earned cash?

Even though it makes intuitive sense not to want to buy stocks at all-time highs or to buy bonds with rates near all-time lows, the reality of what doing so might mean for your portfolio is actually quite different. Not too long ago, my friend, Ben Carlson, looked at the hypothetical results of someone who began investing in the early 1970s, but bought only at major market peaks.

(from Ben Carlson)

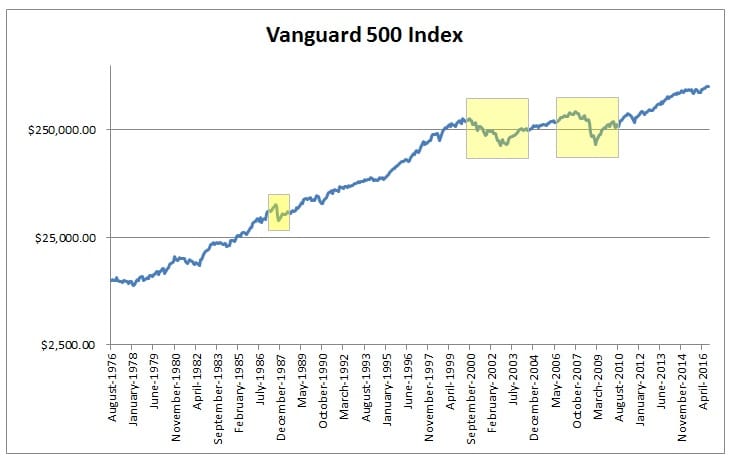

While this hypothetical individual did suffer through some pretty nasty drawdowns on his investments, the fact that he diligently saved and periodically invested more capital, – not to mention never once selling, – meant that his investments grew to over $1.1 million by the end of the 40+ year time span, according to Ben’s calculations. While this illustration assumes a lot about human willpower, the evidence is pretty clear. Just consider the 40-year graph of the Vanguard S&P 500 Index Fund, $VFIAX. A $10,000 investment in August of 1976 with no additional capital commitments but with dividends reinvested ended up worth $627,546 as of September (data from Morningstar):

While they were painful experiences at the time, the last three major market crashes Ben discussed (data for $VFIAX go back only to 1976, so the 1972 crash is not illustrated) ended up being relative blips in the grand scheme of things.

Similarly, investors need not trouble themselves about buying bonds with rates so low. While it is an iron rule of finance that when rates rise, the prices of existing bonds will fall, the math of rising rates actually works out in bondholders’ favor because the bond portfolio will generate higher cumulative returns as maturing bonds are reinvested at higher rates of interest. This should be obvious since the vast majority of returns on bonds has, historically, come from interest received. The effect of rising rates on cumulative returns is aptly demonstrated in this Wall Street Journal graphic:

Here are a few other examples in finance of what many believe, but what are actually untrue:

Buying stocks trading at 52-week lows is not smarter than buying stocks trading at 52-week highs:

Similar to investors not wanting to buy equities when market indices are at all-time highs, many investors are extremely reluctant to buy stocks that are trading at or around 52-week highs. The thinking, of course, is the same: if one buys at the yearly high, he or she is simply setting him- or herself up for disappointment. However, as the brilliant research team at Alpha Architect points out, this ignores two crucial factors: momentum, which in the simplest terms means that stocks that are rising tend to keep rising, and stocks that are down tend to keep going down; and the bias of technical (i.e. price action) over fundamental concerns (e.g. the valuation of the company). The Alpha Architect folks sum up the issue thusly:

Higher risk does not necessarily mean higher reward:

Another myth that prevails in financial circles is that higher levels of volatility and risk are needed to generate higher overall returns. While this may be true from a macro perspective in the sense that equities, while being far more volatile than bonds, but have delivered higher returns than bonds (due to something known as the ‘equity risk premium),’ taking on more risk (as defined by standard deviation, or volatility) does not always equal more reward.

In the high-yield bond space, the opposite has actually been true. In the 20+ years observed, ‘Jake’ at EconomPic Data noted that bonds with higher credit risk (CCC and sub-CCC) have actually delivered lower returns with more volatility than their more creditworthy BB and B counterparts:

The perceived relationship between risk and reward among equities has not held up well on a sector-by-sector basis. As Daniel Sotiroff and I noted last month, over the last 40+ years, sectors of the equity market with lower volatility have actually delivered higher returns:

There are countless other examples in finance of things that are believed to be true, but actually are not. At the very least, they do not seem to be borne out in much if any historical data. The lesson here, of course, is that it when it comes to investing, one should not act on intuition alone, but should rely on data and the accumulated evidence of many years to make informed decisions.

Disclosure: The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Fortune Financial Advisors, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Fortune Financial Advisors, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.