As we think about the amount of savings needed to achieve a financially secure retirement, we can get overwhelmed with thoughts of the unknown – unknown global markets and volatility that could erode our retirement accounts, unknown questions surrounding our future standard of living with no further job related earnings coming in, and for most people, unknown concerns about potential health issues.

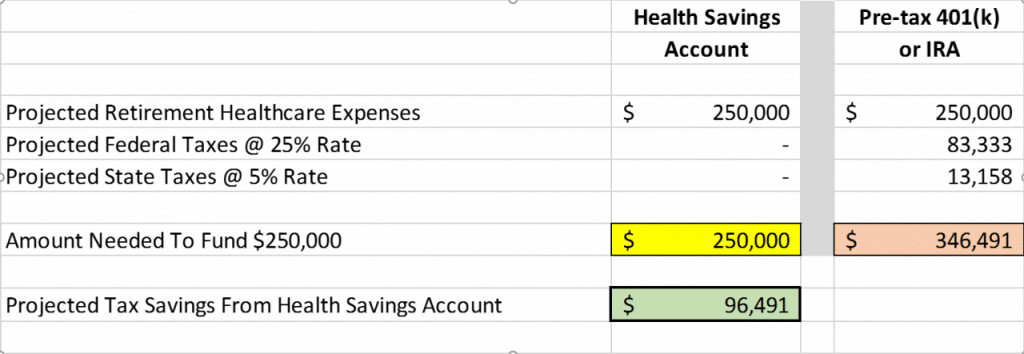

When we look at current data on projected healthcare costs for a couple during their retirement years, it could approach $250,000. Think about that number – it could cost a quarter of a million dollars of our retirement funds just to cover our out-of-pocket healthcare expenses.

To add salt to the wound, it will actually cost more than the projected $250,000 amount if all our retirement funds are in a pre-tax account. This is because every dollar that you withdraw will be taxed at your federal and state marginal rates in the year of distribution.

As an example, say you are in the 25% federal bracket and a 5% state bracket in retirement. In order to net the $250,000, you will need to withdraw a total of $357,143 over the course of your retirement years ($357,143 – $89,286 (Federal at 25%) – $17,857 (State at 5%) = $250,000).

What if you knew of a way to save for these future healthcare costs while enjoying a triple tax-free benefit along the way. The good news is that a retirement-savings vehicle known as a Health Savings Account (HSA) can provide for retirement healthcare expenses much better than your 401(k) or IRA. In addition to the benefits listed below, most people who contribute to a company-sponsored HSA through payroll deductions will save the 7.65% FICA taxes.

- Benefit #1: When you contribute to an HSA, you receive a current year tax deduction.

- Benefit #2: The growth within an HSA is not taxed.

- Benefit #3: Tax-free distributions. When HSA funds are used to pay healthcare expenses in retirement, the distribution is tax-free.

Tax-free trifecta. Now that is a rarity. So let’s look at the requirements to open a HSA. First, you must be covered by an HSA qualified health plan. This means your 2016 plan has a deductible of at least $1,300 for individuals and $2,600 for family coverage. In exchange for higher out-of-pocket costs exposure, an individual can contribute $3,350 to an HSA, and families can contribute $6,750. Those over the age of 55 can contribute an extra $1,000 per year.

So let’s look at the comparison of paying for the projected $250,000 in retirement healthcare costs between an HSA v. a 401(k) or IRA.

Many companies will also contribute annually to an employee’s HSA to incentivize participation in a plan, because employers are realizing large savings on their healthcare premiums. “A lot of people don’t think about how to save for health care in retirement, yet it’s one of the major expenses people will have,” according to Roy Ramthun, president of HSA Consulting Services in Silver Spring, MD.

Here are several ins and outs of an HSA:

- You can rollover HSA funds from year to year. This is unlike a Flexible Spending Account (FSA), where you either use it or lose it from year to year.

- Your HSA is not hitched to your employer whereas your 401(k) plan is.

- Most HSA plans now offer a wide range of investment options to choose from.

- HSA dollars are not shielded from creditors in all states. In the rare incident where a successful lawsuit results in an award higher than policy limits, the HSA could be subject to the settlement.

- You should plan to spend your HSA the best you can prior to death. That’s because when you die (or you and your spouse if married), the HSA becomes fully taxable to your named beneficiary or your estate. Unlike an IRA, there is no “stretch” provision.

A Health Savings Account has one more potentially enormous future benefit. That is, HSA dollars are not required to be withdrawn in the same year as the underlying healthcare expense. Thus, some people have chosen to pay for current healthcare expenses with after-tax funds, while keeping these receipts for decades. Down the road they withdraw these amounts from their HSAs tax-free to spend as they please – on a trip, boat, etc.

Federal guidelines governing Health Savings Accounts can be found in IRS Publication 969.

As in any analysis of building retirement wealth, there are many variables to consider in your decision. Variables such as current health issues, family longevity history, outside assets available to fund retirement, marital status, income level, and tax bracket (to name a few) are critical to your analysis of how to allocate funds for retirement healthcare costs.

We encourage you to contact Fortune Financial to let us help determine options best tailored to your unique needs.

The information provided in this publication is for general information only, and is not intended to provide specific recommendations.