Whenever there is a major move in the value of the dollar, you will likely hear talking heads recommend one adjustment or another to your portfolio, whether it is to compensate for, or take advantage of, the opportunity presented. For example, because a far greater percentage of revenues are earned overseas by large cap companies, you will likely hear that a tilt toward large caps is warranted when the dollar weakens. Conversely, when the dollar is strengthening, you will probably hear a recommendation to tilt toward more domestically-oriented small cap stocks. However, when performing a thorough analysis of past dollar cycles, it is not clear that moves in the dollar really warrant major repositioning within the domestic portion of a portfolio.

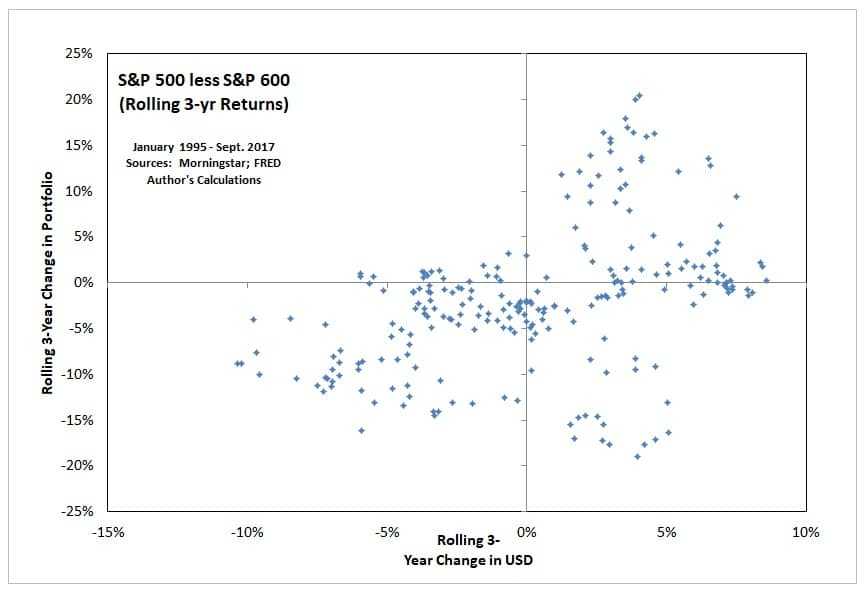

Let us begin with an examination of the difference in returns between large cap and small cap stocks during different dollar cycles. As stated above, the when the dollar is weak, conventional wisdom states that multinational large cap firms (such as those represented by the S&P 500 index) would benefit more than small companies (as represented by the S&P 600 index). Yet over the last twenty-plus years, it has actually been the reverse: when the dollar has strengthened, large cap firms have actually outperformed smaller firms:

To be sure, over this time period, there have been only two major dollar cycles: a period of great strength during the late 1990s, and a period of great weakness during the early 2000s. Therefore, to get a longer-term picture, I performed the same analysis on the Russell 1000 large-cap index and the Russell 2000 small cap index, both of which have histories going back to 1979. The results were even less compelling: regardless of what the dollar did, large caps or small caps alternated in terms of superior performance:

To be sure, the natures of the indices have changed a lot over time, with technology stocks taking the lead in the majority of the major domestic stock indices. Therefore, perhaps instead of trying to test large versus small, a better test might be to compare companies of similar size but within industries with much different revenue sources.

To help with this test, I took data from SPIndices.com to calculate the implied percentage of revenues derived abroad for each sector within each category of size. We can see from the graph that revenues for utilities and telecommunications are generated almost entirely domestically, whereas revenues for information technology are about even as far as being earned domestically or abroad:

To test the sensitivity of foreign revenue earners to dollar moves, we could compare, for example, technology stocks versus utilities. However, as items of necessity, utilities are less cyclical, so I chose instead to compare technology stocks to consumer discretionary stocks, since both are more cyclical in nature, and a comparison would likely yield more useful results from a portfolio positioning standpoint. Furthermore, – whether large cap, mid cap, or small cap, – technology stocks earn a lot of their revenues abroad, while consumer discretionary stocks, by comparison, tend to generate more revenues domestically.

However, as with the test of large versus small stocks, the results were mixed. Comparing large technology stocks to large consumer discretionary stocks revealed that there is no discernible advantage to multinational IT firms when the dollar is weak, or for domestic consumer discretionary firms when the dollar is strong. This holds true for their smaller counterparts, too. First, the large companies:

And now the small companies:

Given these results, the overwhelming conclusion, in my opinion, is not to worry about the dollar’s impact on the domestic components of your portfolio. As I have written before, currency moves are much more important to the foreign component of an investor’s portfolio. The rest appears to be little more than noise.