My favorite chapter in Peter Lynch’s Beating the Street is titled, “Blossoms in the Desert: Great Companies in Lousy Industries.” In this part of his book, Mr. Lynch writes:

“I’m always on the lookout for great companies in lousy industries…As a place to invest, I’ll take a lousy industry over a great industry anytime. In a lousy industry, one that’s growing slowly if at all, the weak drop out and the survivors get a bigger share of the market. A company that can capture an ever-increasing share of a stagnant market is a lot better off than one that has to struggle to protect a dwindling share of an exciting market.”

It goes without saying that many of the ‘blossoms’ that Mr. Lynch described in his book are perhaps no longer applicable as examples of ‘great companies in lousy industries’ as a lot has changed in the quarter-century since Mr. Lynch’s book was published. The goal of this article, then, is identify a few current ‘blossoms in the desert’ with the purpose of updating Mr. Lynch’s thesis a bit.

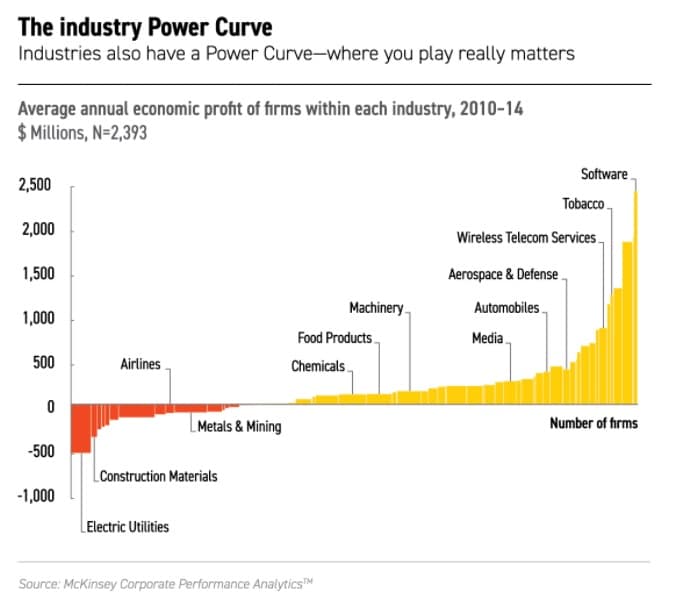

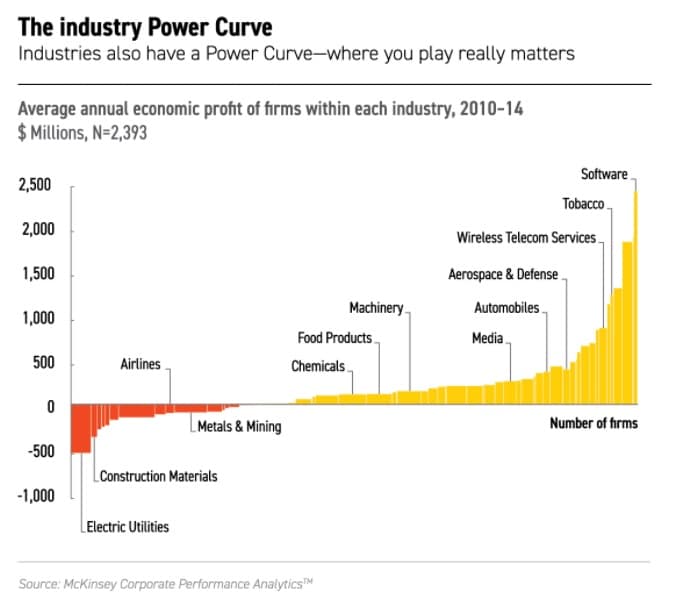

The first order of business is to identify the lousy industries that Mr. Lynch describes. To do this, I took a few of the industries that find themselves on the losing end of what McKinsey calls the “Industry Power Curve“:

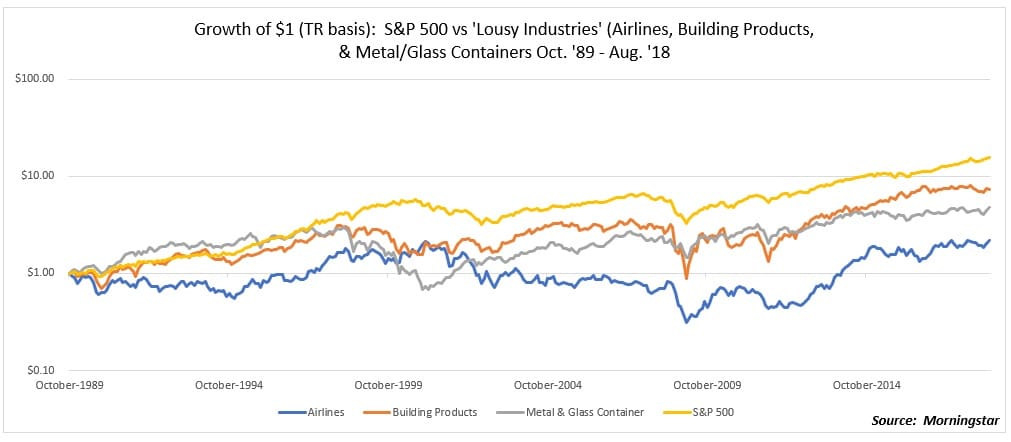

The three lousy industries I chose to look at are airlines, building materials, and metal & glass containers. To demonstrate just how lousy these industries have been, I charted their multi-decade performance versus the S&P 500. Each underperformed the market by a fairly wide margin:

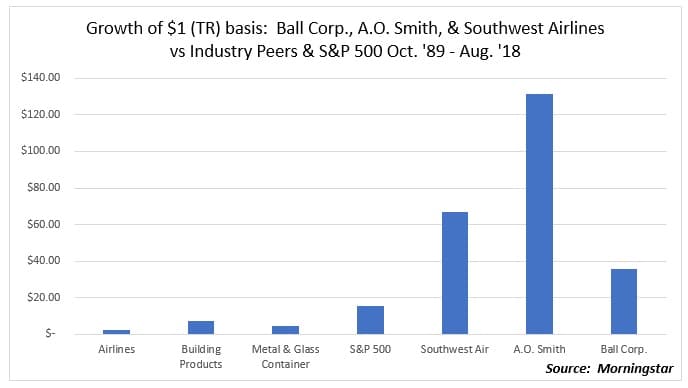

Yet, just as Mr. Lynch stated, there were ‘blossoms’ in each of these industries that handsomely rewarded investors brave enough to look past the industry factor. Consider the cases of Southwest Airlines, A.O. Smith (building products), and Ball Corp. (metal & glass containers). In each instance, the shares of these ‘blossoms in the desert’ not only crushed their industry peers, but also the wider market:

So what exactly made these companies so great despite being players in weak industries?

The performance of Southwest Airlines is well-documented; Mr. Lynch wrote about it at length in Beating the Street, and Professor Jeremy Siegel also dedicates a good portion of his book, The Future for Investors, to the remarkable airline. In fact, Professor Siegel points out that Southwest Airlines is the only company to have bested the returns of Warren Buffett’s Berkshire Hathaway since 1972. Some of the reasons Mr. Lynch and Professor Siegel list as catalysts for Southwest’s success is the measured pace of its growth, its reliance on one model of airliner (Boeing 737) and the efficiencies and savings from that, as well as its great relationship with both its employees and passengers. Building on the corporate culture that is a legacy of its legendary former chairman, Herb Kelleher, Southwest Airlines has become not just a great company in a lousy industry, but one of the best-run companies in the world.

Ball Corporation, which no longer makes the famous mason jars that still bear its name (the brand has since been acquired by Newell Brands), is the world’s largest producer of metal cans, which make up the lion’s share of Ball’s revenues (Ball also has some exposure to the aerospace industry). Even though the can industry is one of little growth and small margins, Ball has succeeded by expanding its global operations at a measured pace, always with an eye on profitability. In addition, it is worth noting, as Morningstar does in a recent research note, that 10% of Ball’s shares are owned by its employees, which creates a powerful incentive for them to ensure the success of the company. This has no doubt been a factor in the company’s success.

A.O. Smith is a leading manufacturer of water heaters and boilers for both commercial and residential use. The company has grown from a small manufacturer in Milwaukee to one with a global footprint; in fact, A.O. Smith reports that now 43% of its 2017 sales originated outside the U.S. The company has focused on high-efficiency products, and, in addition to its traditional distribution channels, A.O. Smith has adeptly leveraged online retail platforms to market its products. A.O. Smith has proven itself to be nimble in navigating a competitive global marketplace, all the while steadily growing and maximizing shareholder value.

For these companies to have succeeded in tough markets as they have, each has had to adapt to changes in globalization, technologies, and survived some periods of very tough economic circumstances. That each has done so well is a testament to the skilled management, corporate culture, and adaptability that seem to set them apart from their peers. Their success serves as validation of the Lynch philosophy.

Note: The author owns shares of A.O. Smith. Clients of Fortune Financial own shares of Southwest Airlines.