In previous posts, I have written about the utility of pairing low or minimum volatility strategies with momentum to create a superior dual-factor portfolio (see here, here, and here). This is, I think, a very simple and easy portfolio strategy to implement, particularly now with the advent of low-cost factor-based ETFs.

Another way to implement the portfolio is to utilize sector pairs, and, in my opinion, an obvious combination is consumer staples, which typically exhibit low volatility characteristics, and information technology, which oftentimes over the past ~30 years have exhibited momentum characteristics.

This can be seen why comparing the return series of a 50-50 Low Vol / Momentum barbell with a 50-50 Consumer Staples / Info Tech barbell:

Given the tight correlation, I wanted to explore this idea more. Available data for the S&P 500’s sectors go back a little further than comparable factor indices, so I took the concept back to 1990. One can see that when compared to the parent index, consumer staples and technology often diverged, with one outperforming while the other underperformed:

The biggest period of diverging returns was of course the tech bubble and its aftermath, but there have been similar, albeit less pronounced, periods before and since. This makes sense, as consumer staples are typically defensive in nature, and tend to do better when the economy is stumbling, and the market is shaky, while technology is more cyclical.

By combining the two, we can see that the barbell portfolio typically suffers shallower and much less frequent periods of underperformance compared to either sector individually:

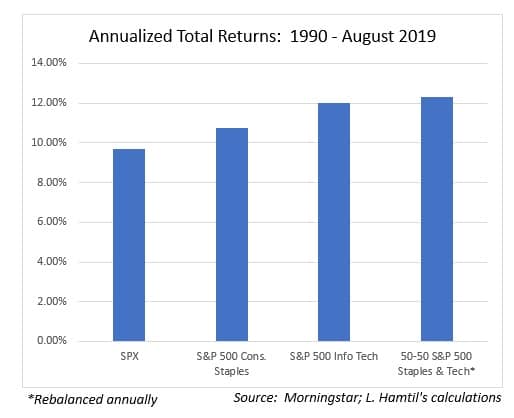

Since 1990, information technology has been the best performing S&P 500 sector, generating annualized total returns of 12.01% through August. Consumer staples outperformed the S&P 500, too, but trailed technology by a fair margin, returning 10.74% annually. However, combining the two in a barbell resulted in a superior return of 12.32% annualized:

Furthermore, technology’s superior return came at a cost, with a much greater maximum drawdown (~80%), and much higher volatility, so the Sharpe ratio for the sector (its risk-adjusted return) was actually lower than the S&P 500’s. Not only did matching technology with consumer staples improve the results on an absolute basis, it actually generated a higher Sharpe ratio than the market and consumer staples, which is somewhat extraordinary:

So, there you have it: yet more evidence that the dual factor approach of combining low volatility with momentum is worthwhile, and that there are several ways to implement it.