One of my favorite investment themes to explore is the role that industry dynamics play in company performance, and, therefore, investment performance. For example, I discussed here the importance of specific industry economics as they relate to profitability and returns on investment. More recently, I touched on the critical role that industry structure plays in the success of many “compounders”, which are oftentimes industry consolidators. This post is an attempt to tie these things together as I identify what I would consider to be the traits of an ideal industry, including a case study of one such industry I believe checks all the boxes, so to speak.

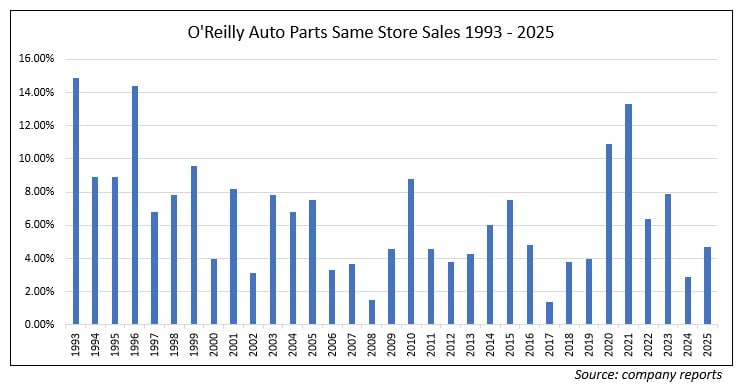

- The product or service is economically agnostic, meaning that it can thrive in good times and bad; it is not overly dependent on the overall economic cycle to thrive. One such example is auto parts retail. When the economy is growing, there are more miles driven, which means more repairs and more replacement parts. When the economy is in a downturn, new car sales lag, and drivers opt to maintain the cars they currently have, thus leading to more demand for replacement parts. This resilience can be seen in the same store sales growth of industry bellwether O’Reilly Auto Parts, which has reported positive same store sales growth every year since going public in 1993. Despite multiple economic downturns along the way, including the financial crisis of 2007 – 2009, same store sales growth continued:

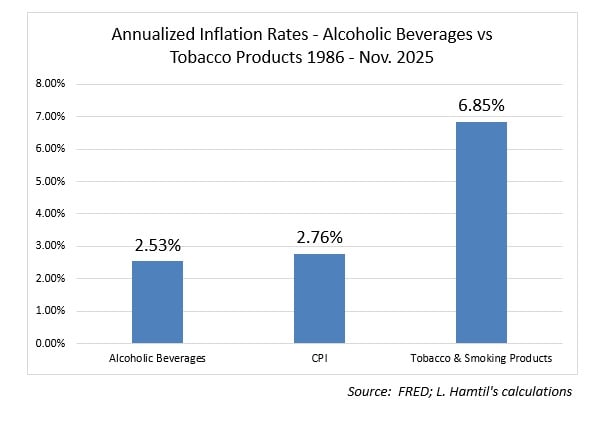

- The industry benefits from strong pricing power, meaning that the industry incumbents are price makers, not price takers, and, ideally, can raise prices faster than inflation. An example of an industry with strong pricing power is tobacco, which has historically raised prices faster than overall inflation, thus resulting in outsized profit growth relative to consumer staples broadly; the opposite would be alcoholic beverages, which have failed to pass on costs at even the rate of inflation over the past few decades:

- The product or service is mission-critical, but a small cost overall. It is a good place to be when your product or service is mission-critical, but a small cost of the overall project, product, etc. These niches tend to have a lot of pricing power because there is a high cost of failure and so substitute lower-priced competition is often not even considered.

- The industry benefits from a high incidence of recurring revenue. To see better the value of recurring revenue it may be instructive to look at an example of an industry with virtually none of it. One of the opportunities Wayne Huizenga identified when he started AutoNation in the 1990s was that ~75% of all auto dealership customers did not return for a second, let alone a third, purchase. By consolidating several hundred dealerships and focusing on customer service as well as less discretionary customer spending on maintenance, he sought to alleviate the severe customer churn the dealerships faced. It is no wonder that selling cars is a cutthroat business when three out of every four of your customers are turned over frequently. Investors place a premium on businesses with more easily predictable revenue growth, and with good reason.

- There are either barriers to entry or barriers to scale. I have written in the past about several industries with barriers to entry that are more durable than others. These would include tobacco, where government regulations regarding advertising and product enforcement make it very difficult for new players to enter the marketplace, or railroads, where long established players have already built out networks that cannot be duplicated on real estate that is not for sale. Less discussed are barriers to scale in industries where new players may enter the market more or less at will, but struggle to achieve any semblance of economic scale. An example of this would be trucking, an industry in which new drivers can offer their services with the proper licensing and a tractor-trailer at his or her disposal and gain business through freight brokers. However, these small players face high hurdles when it comes to the capital requirements for acquiring more trucks, train and keep employees (some estimates show employee churn as high as 90%), and maintain facilities. These are real barriers to scale that insulate the largest players in the market.

- The industry is benefiting from strong secular tailwinds. With all due respect to Peter Lynch’s famous preference for no growth industries, I believe strong growth is necessary to make an industry stand out. By this I am not referring to strong but short-lived cycles but rather to those trends that play out over many decades. One such megatrend is the migration of people to the South, which has been playing out for decades and still shows no signs of slowing down. You can read more on that topic here.

A case study: Pest control

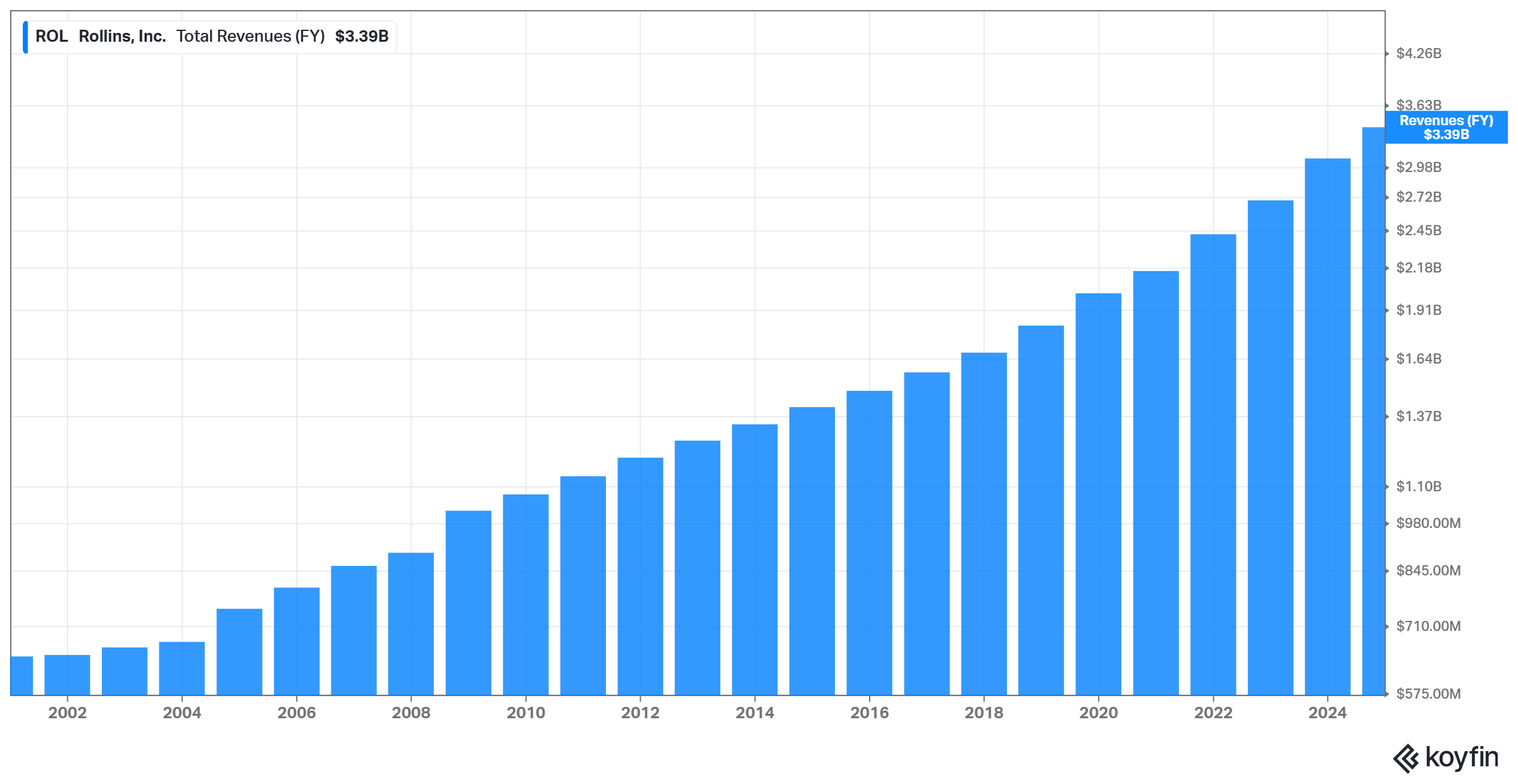

An example of an industry that arguably ties all of these features together is pest control, which has grown without interruption for decades, and at a rate faster than GDP. Because official industry data are hard to come by (the Federal Reserve database ends in 2022, sadly) we can look at the results of Rollins, Inc. owner of Orkin as well as several other leading pest control brands. One can discern from the chart that revenues grew solidly through both the financial crisis and the COVID pandemic. That satisfies our criterion for being economically agnostic.

The pest control industry is mission-critical, featuring strong pricing power and recurring revenue, which satisfies our second, third, and fourth criteria. Rollins employs a CPI+ pricing model, meaning they consistently charge their customers a margin above inflation, which keeps their margins healthy. Recurring revenues are a stated ~75% of the business, so revenue streams are very predictable and consistent. Moreover, pest control is non-discretionary (your restaurant has to pass that health board exam, for instance), because the cost of it is very low compared to the cost of being closed for business due to an infestation. This is highly supportive of pricing power.

While there are relatively low barriers to entry in pest control (there are estimates of anywhere from 15,000 to 20,000 pest control providers in the US alone, the vast majority of them with revenues less than $50,000,000), there are several barriers to scale. Pest control is inherently a classic route-density business. There are only so many locations a technician can reach in any one day, so schedulers will try to assign as many jobs as possible within a certain area so that technicians spend most of their time providing services as opposed to driving from job to job. This means that larger players with more resources will have an advantage as they deploy more capital on route optimization software, as well as more trucks and technicians to provide services. Additionally, they should become acquirers of choice as smaller players seek to combine forces with the larger players rather than try to scale themselves. This satisfies our fifth criterion.

Finally, pest control benefits from strong secular tailwinds such as the movement of people to the southern states (warmer weather means more bugs, especially termites), and that means more pest control demand. Furthermore, the gradual rise in temperatures means winters with fewer deep freezes, which also means more bugs, and thus more eventual demand for pest control services. When combining these things with overall increases in household formation and rising consumption at hotels, restaurants, etc., it seems like the industry has a very bright future ahead of it.

Disclosure: At time of writing, both the author and clients of Fortune Financial Advisors, LLC maintained positions in O’Reilly Auto and Rollins, Inc. The information provided in this article relating to stock examples should not be considered a recommendation to buy or sell any particular security. Any examples discussed are given in the context of the theme being explored.