I was introduced to the term ‘industrial staple’ while recording the Inside the Factory episode of the Preferred Shares podcast. In that episode, our anonymous guest enlightened us about the various mission-critical items that make a factory run. These would include services such as sanitation and pest control, as well as high-quality lubricants, seals, and gaskets. These somewhat mundane things always seem to fly under the radar because most of us experience the world as consumers, not as insiders in the industrial world, so we remain largely ignorant of the things that literally make the world run, and provide us with what we consume.

This idea of an industrial staple came to mind this week when it was announced that Martin Marietta Materials would be combining with Lhoist North America in a deal valued at around $13.5 billion. The main attraction of Lhoist North America for Martin Marietta is its network of limestone quarries with some 200 years of useful life. While I was familiar with Martin Marietta’s core business of selling construction aggregates, I was not at all familiar with the economics of and use cases for limestone.

As it happens, limestone is one of those base elements so critical to so many different things, from water treatment to steel manufacturing. As Martin Marietta CEO Ward Nye put it on the conference call outlining the deal:

“The Texas Department of Transportation requires lime to stabilize clay-rich soils and strengthen road-based materials, establishing a specified source of demand that is highly synergistic with our aggregates base course product offering. Beyond infrastructure and construction applications, lime is an essential input in steel production where it serves as a fluxing agent to remove impurities and improve both yield and finished product quality…Lastly, lime plays a critical role in water and wastewater treatment, supporting pH control, softening and contaminant removal to meet regulatory standards.”

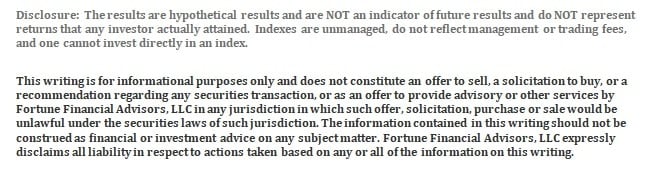

Because limestone is an essential ingredient for so many different things, some of which are cycle-agnostic such as water treatment, demand is fairly steady. Also, like aggregates, limestone is not easily substitutable if at all, and the economic value is less than the cost of transportation, so local quarries operate much like local monopolies. This leads to strong pricing power, which has surpassed both aggregates and overall inflation over the last ~35 years:

Given these characteristics, as well as the overall economic backdrop of reindustrialization and infrastructure spending, it is not surprising that limestone quarries are attracting attention.

Industrial Gases

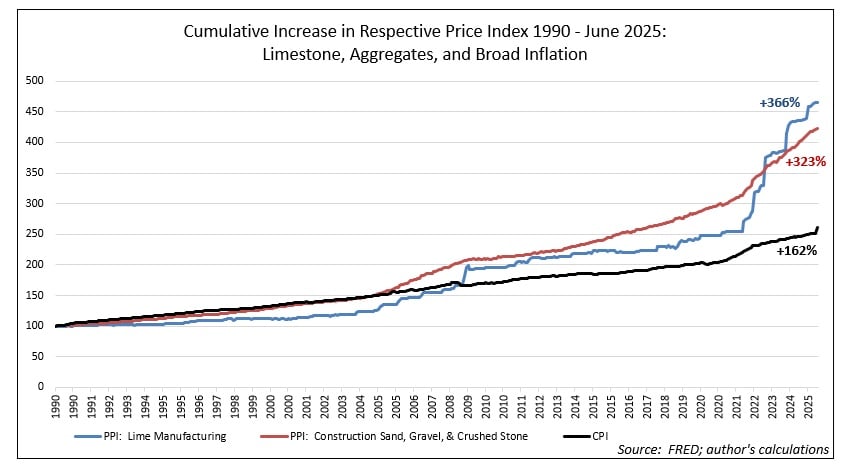

Industrial gases are another critical input for so many different things, from helium in semiconductor manufacturing and specialty welding to oxygen in steelmaking, rocketry, and medicine. The industrial gas sector has always enjoyed strong pricing power due to the critical nature of its products as well as its long-term take-or-pay contracts. However, that pricing power has been greatly strengthened by consolidation in the industry over the last quarter century, resulting in the top three players accounting for roughly 75% of total industry revenues.

Now, with the growth in rocketry as well as the onshoring of major semiconductor fabs, industrial gases as important as ever.

Bearings

Modern bearings trace their lineage to the 18th century when Welsh inventor Philip Vaughn was awarded the first patent for a bearing. Over time, the concept became adaptable to pretty much anything with a moving part that needed reduction in friction. By the 1940s, bearings had become so critical to modern industry that the targeting of German bearing factories became a top priority for Allied air forces during World War II. Now, bearings can be found in everyday things like washing machines and automobiles to complex rockets and satellites. Because they are essential to the smooth functioning of increasingly complex – and thus expensive – machines, bearings fall into that category of industrial components that constitute a low absolute cost of a machine, but represent a high cost of failure if they do not function properly. Therefore, it is less likely that buyers of bearings will worry too much about the price paid.

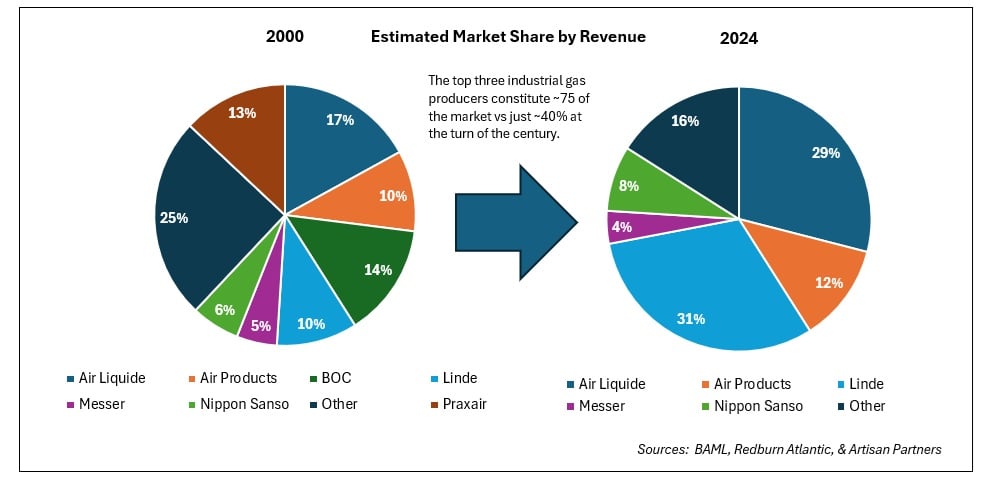

However, a distinction should be made between common ball bearings, which are more of a commodity product, and tapered roller bearings, which are highly engineered and most likely to be found in high-end applications such as wind turbines, jetliners, and heavy machinery. The difference in pricing power can be observed in the chart below, which plots pricing data for the two bearing types less the common input cost of iron and steel:

When input costs rise, implied margins for tapered roller bearings fall less and recover faster than those for common ball bearings. Not all industrial staples are created equal.

Gaskets

On January 28th, 1986, the space shuttle Challenger blew up shortly after launch with all crewmembers killed. The culprit? A faulty $10 O-ring gasket that had failed. This tragedy highlighted the importance of high-quality sealing devices to many applications, including space travel. Gaskets, like bearings, are high cost of failure items that do not represent a large portion of the overall cost of a product or machine. As such, they command a lot of pricing power, even during economic downturns. Over the last ~40 years, there has yet to be a year-over-year decline in the price index for manufactured gaskets and sealing devices:

These are just a few of the many industrial staples that keep the world fed, moving, and exploring. I certainly now have a greater appreciation for these humble items that play such vital roles in our daily lives.

Disclaimer: Any reference in this post to stock examples should not be considered a recommendation to buy or sell any particular security. Any examples are given in the context of the theme being explored.

Both the author and clients of Fortune Financial own shares of Martin Marietta and Linde.