In a recent post that created a bit of a stir, I outlined a few reasons why equity investing hasn’t always yielded stellar results in all countries, and that much of the idea of ‘stocks for the long run’ comes from the Anglo-Saxon countries in general, and from the United States in particular.

Continuing with that theme, I thought it would be worthwhile to dig a little deeper to show just how stark some of the differences are between the primary Anglo-Saxon markets (the US, Canada, Australia, the UK, Ireland, and New Zealand), and their global contemporaries.

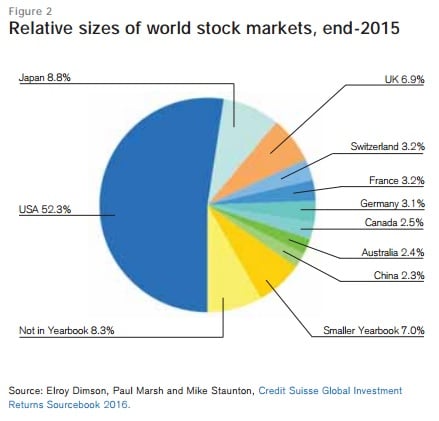

The World Bank keeps a fairly detailed database of listed companies per country. While it is not complete, – there is no data for Italy, for example, – it will serve for our purposes. Of the more than 45,000 listed companies in the World Bank database, more than 27% reside in the Anglo-Saxon countries. Lest you think that the US is responsible for most of these, you may be surprised to find out that the US has only about 700 more listed companies than its northern neighbor, Canada.

While Canada’s economy ranks 10th in the world, its stock market value is ranked 7th:

Compare this to Germany: the German economy ranks 4th in size, – more than twice the size of Canada’s, – yet its stock market is marginally larger than Canada’s. What is more, Canada boasts almost 3,700 listed companies, whereas Germany has fewer than 600.

A similar contrast can be made between France and Australia. Australia’s economy is half the size of France’s, yet there are almost 2,000 listed companies in Australia, versus only 550 in France.

Not surprisingly, the market value of listed stocks in Anglo-Saxon countries has tended to exceed GDP recently; at the end of 2014, the World Bank reported that Canada, the US, and the UK all had market cap-to-GDP percentages greater than 100%, while Australia’s was close to 100%. By comparison, the stock markets of Germany and France had market caps valued much less than their respective GDP.

What can explain this disparity between the Anglo-Saxon countries and major economic powers like France and Germany?

In an older edition of the European Economic Review, Italian researchers sought to explain this phenomenon by looking at how various countries view the stock market as a source of capital for corporate operations:

The importance of the stock market in financing investment, monitoring companies and reallocating corporate control varies greatly among developed capitalist economies. In Anglo-Saxon countries, the stock market plays a central role in these functions, whereas in most Continental European countries and in Japan banks are much more prominent in financing and monitoring companies, and often play a major role in reallocating control as well…

In most of Continental-Europe only a few large, historic corporations are listed, while in Anglo-Saxon countries resort to the market is very widespread and tends to occur early in the life-cycle of a company.

Given this disparity between the Anglo-Saxon nations and much of the rest of the world, it is interesting to ask the question whether the stocks available to invest in for most non-Anglo-Saxon countries are even the best investment opportunities in that particular nation. With this in mind, let us examine the case of Brazil.

Brazil ranks ninth in the world in terms of the size of its economy, yet there are only 351 listed companies. Globally, this ranks Brazil 15th in the wrold in terms of market value of its stock market. At less than $1 trillion in value, it is much less than both Canada’s and Australia’s markets. What’s more, the market value of its public companies is much less than the value of its private companies.

Last June, S&P Capital IQ put together a fascinating report on the differences between public and private companies in Brazil. What they found was that almost across the board, private companies had much great margins than their public counterparts:

The biggest differential can be seen in Energy, Materials, Financials, and Utilities. This, S&P concludes, is not surprising, given that these sectors

“are all typically subject to more government regulation and control.”

One might be tempted to explain this away by pointing out that because of state control of many of the country’s resources it is pointless to analyze the private companies in those same industries. While that may be true in the Energy sector, it is important to note that, by revenue, the size of Brazil’s private financial firms is much greater than the public firms, while among Utilities and Materials private firms are not inconsiderable:

In sum, I think it is unwise to think of stock markets around the world to be very similar to what we are accustomed in the Anglo-Saxon sphere. While I agree that having significant exposure to foreign markets is key to a diversified portfolio, one must do so while having tempered expectations because, for whatever reasons, – be they legal, cultural, or financial, – many of the best investment opportunities abroad may be closed to you because the founders and operators do not rely on public ownership for financing and growth.