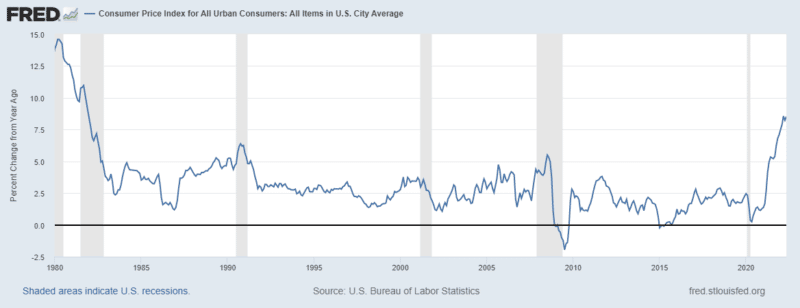

Inflation is now front and center in the minds of investors as domestic measures of consumer prices reach levels not seen in a generation:

This is obviously a sea change for investors long accustomed to the benign inflationary environment that has prevailed with little interruption for several decades.

Since I have written on the topic and its impact on financial assets on several different occasions I thought it would be worthwhile to revisit some of those ideas now that inflation has returned.

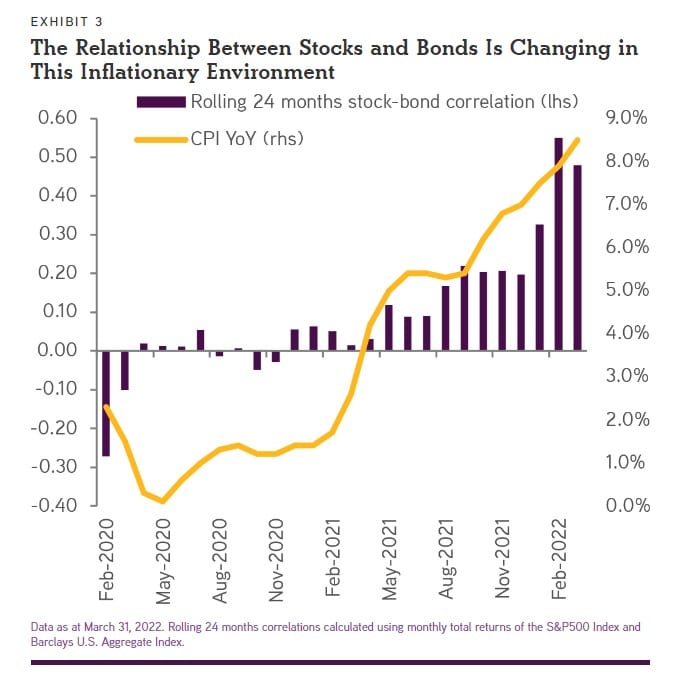

- Inflation drives up the correlation of long-duration financial instruments

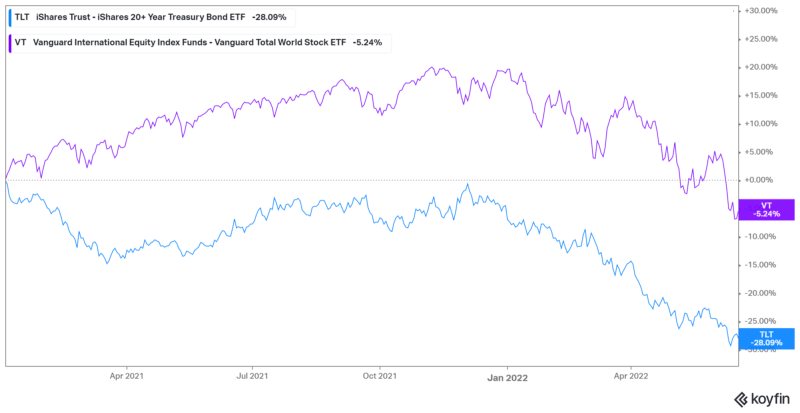

As we discussed in 2016, and putting aside technical differences, stocks and bonds are, when inflation strikes, not all that different except in terms of duration as both represent claims on future income streams. With similarly high duration, the effect of a long, benign inflation regime, long-term bonds in particular can subject holders to equity-like volatility. This can be seen by the fact that since the end of 2020, long-term treasurys, as measured by the iShares 20+ year treasury ETF (TLT), have declined roughly 28% through mid-June, versus just a ~5% decline for Vanguard’s Total World Stock Market ETF (VT):

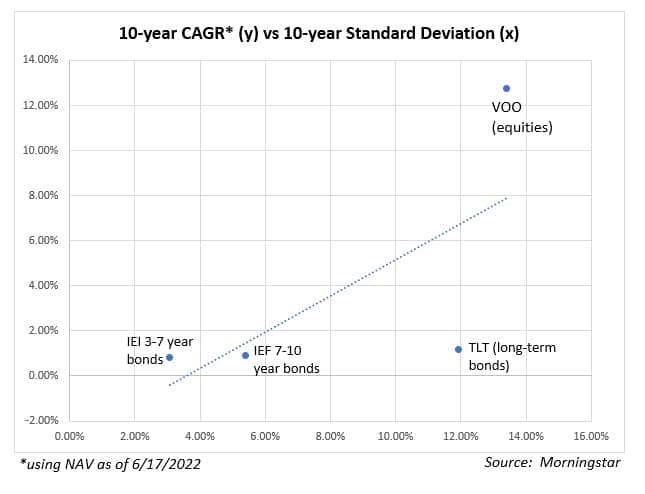

As a result of this inflation-induced carnage in bond markets, long-term treasurys have only barely outperformed their shorter-duration peers but with volatility only slightly less than stocks:

It is for this reason that I think it is helpful for investors to think of their asset allocation not just in terms of asset class, but also in terms of duration, since inflationary forces drive the correlation of long-duration instruments toward 1, greatly reducing the benefits of traditional asset allocation practices accustomed to low inflation (chart from KKR):

2. Inflation shortens time horizons

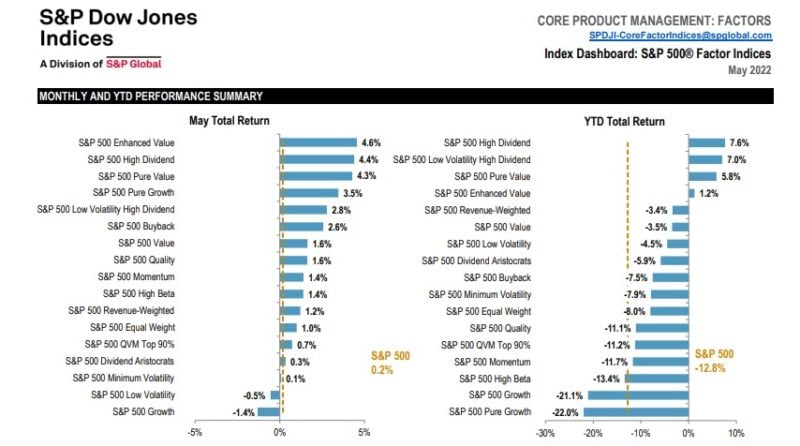

While inflation tends to harm long-duration assets the most, it seems to do so to the benefit of lower duration assets. This is because investors tend to be more concerned with immediate returns on their capital, and are willing to pay less for future income streams. This can be seen in fairly obvious ways, such as comparing cash and short-term bonds with long-term bonds, or commodities with financial assets. Across equities it can be observed by the favorable performance of dividend-paying stocks relative to non-payers; through May, S&P’s High Dividend index was one of the few factor indices with positive returns so far in 2022, outpacing Pure Growth by almost 30% (chart from S&P):

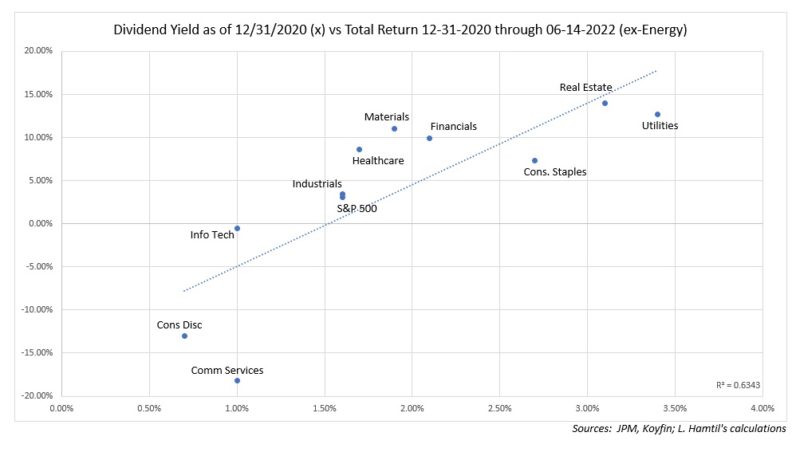

Along those lines, it is interesting to note the strong relationship with starting dividend yields at the end of 2020 when inflation was just starting to pick up some team and subsequent performance through mid-June (Note: I have excluded Energy from this illustration as its strong performance can obviously be more clearly attributed to high energy prices.):

3. Energy stocks are valuable diversifiers

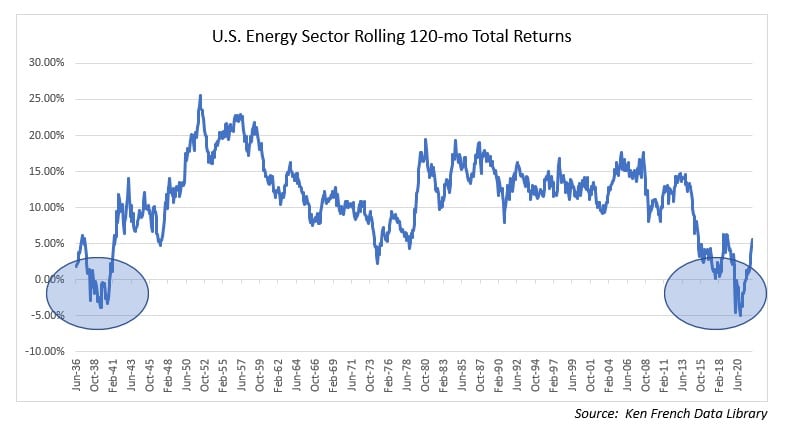

In 2019, energy stocks were mired in a long, deep bear market, and many were echoing Jeremy Grantham’s argument that divestment from fossil fuel equities would not harm investors’ long-term returns. I took the opposite view arguing that energy stocks were worth holding onto as they provide investors with what have been one of the surest hedges against inflationary pressures.

As the pandemic induced mobility freeze drove energy prices to negative levels in some cases, those of Mr. Grantham’s mind seemed vindicated as rolling energy stock returns were weaker even than at any point during the Great Depression:

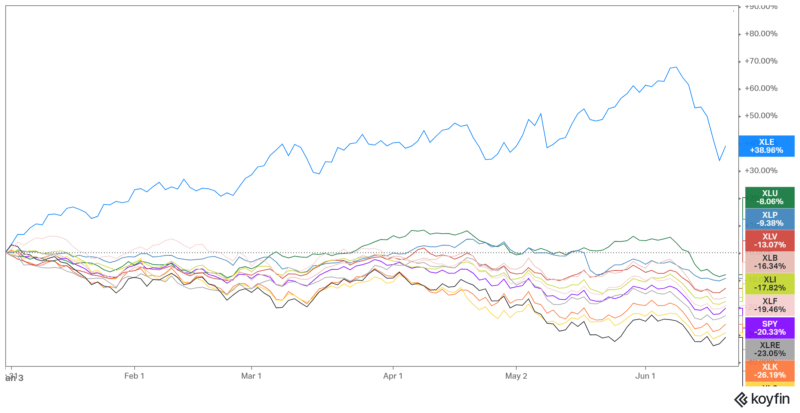

The world has obviously changed a lot since then, with demand for energy having rebounded strongly, while supplies have yet to catch up, driving up energy prices to levels not seen in years. Those who held onto their energy shares have been rewarded for their patience as the energy sector is the only sector with positive total returns so far in 2022:

I suppose that if you use a long enough time horizon that Jeremy Grantham might indeed be right that owning energy shares may not matter to long-term portfolio returns, but 2022 is a reminder that long-term results can be achieved only by surviving the short-term, and that means having a portfolio sufficiently diversified to do so. The energy crunch many are unfortunately seeing in Europe and elsewhere is a reminder that fossil fuels will be with us for some time to come, and the companies who produce them should continue to provide some level of inflation hedging so long as they are.

It is impossible to predict how much longer inflation will continue to be the driving factor in markets, but its return after a long absence is a reminder that markets can often fall prey to false security as we think back to the recent past and assume those conditions will prevail in perpetuity. It is in some ways a welcome reminder that prudent portfolio construction is a delicate balancing act that should strive to be as agnostic about the future as possible since it seems that the risks we too often discount are those that present the gravest dangers.