In April 2018, less than one year into what would become a major secular bear market for tobacco, I suggested that the decline in tobacco stocks was likely to be brief; it is fair to say I could not have been more wrong as the subsequent period has marked the worst bout of underperformance for the category since the TMT bubble of the late 1990s:

Secular market cycles are often driven by sentiment; a new technology or major innovation can drive up the shares of a major industry for years at a time, just as they have previously with airlines, PCs, the internet, and so on. Tobacco, I would argue, is no different, except that secular shifts in sentiment are not driven by innovation so much as they are by regulatory or litigation-related fears. It is no coincidence, for example, that the two most recent periods of major tobacco underperformance in the last several decades have been driven largely by a huge compression in multiples, the result of serious litigation (1998 – 2003) and regulatory (2017 – present) challenges.

Now I should take a moment to clarify why I am singling out Altria in this post. For one, Altria is a more or less pure play on the U.S. tobacco/nicotine market so it makes for easy analysis when looking at the industry and its prospects. Secondly, it is a kind of battleground stock in a controversial industry, so the data are timely and relevant.

With that being said, some might argue with me about why the stock has performed so poorly the last several years. Perhaps it is related to a deterioration in business fundamentals? If that is the case, you certainly cannot find evidence of it in company results; since 2009, the first full year in which Altria was fully separate from Philip Morris International (PM) and thus a pure play on U.S. tobacco, the shares have outperformed the S&P 500 by a healthy margin, a result almost entirely driven by earnings and dividend growth. By comparison, since the end of 2017, the entirety of the underperformance was driven by multiple compression, as earnings growth and dividend growth were little deviated from the longer-term trend, and in fact surpassed the index’s fundamental results:

Now, to be fair, there are legitimate concerns about the sustainability of the industry since there is a long and on-going secular decline in the smoking rate, and the lion’s share of Altria’s revenues are tied to combustibles. This fear is in part driven by an acceleration in adoption of reduced risk products such as vaping which threaten to disrupt the profit pool Altria enjoys by offering an enjoyable alternative nicotine delivery method that purports to be safer than smoking. Proponents of this argument will point to a huge increase in vaping as a percentage of the nicotine revenue pool the last several years as evidence of this, yet that analysis misses a key point which is that cigarette revenues have grown in absolute terms despite the heightened competition:

How exactly does this math work? For one, it is yet more evidence of denominator bias at work in smoking-related statistics. For example, the smoking rate is currently as low as perhaps it has ever been, yet this is mostly driven by population growth as the absolute number of adult smokers in the U.S. has declined at a somewhat glacial pace of 1.76% since 1998. This rate of decline has accelerated only modestly over the last decade to around 3%, driven in part by reduced risk products. Simply put, there is still a very large number of people in the U.S. who enjoy smoking and who will pay up for it.

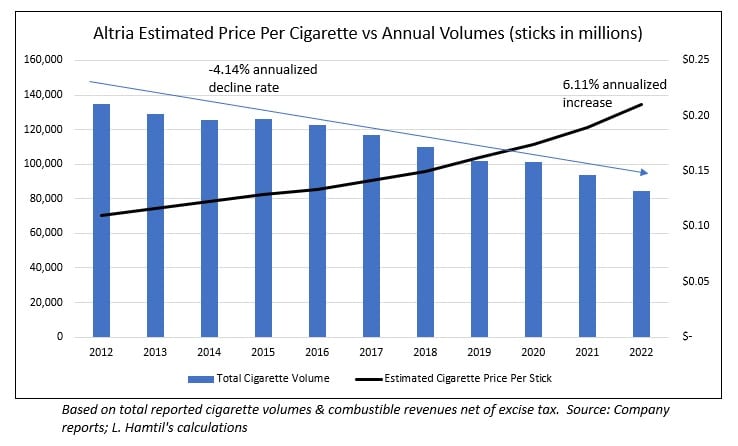

The key then, for Altria and its industry peers is an enormous and almost unrivaled ability on the part of tobacco companies to take price. Over the last decade, Altria’s price taking has amounted to around 6% a year versus a decline in volumes around 4% per year, which loosely corresponds with the ‘quit rate’ cited above:

That math can work in the company’s favor for quite some time, especially given that cigarette prices are particularly affordable relative to incomes in the United States, as Price to Wealth has demonstrated.

Furthermore, smokers are famously brand loyal, which bolsters the company’s ability to take price. For example, Marlboro’s (Altria’s flagship brand) rather dominant market share in combustibles has not been below 40% since 2004:

I think I have demonstrated sufficiently that the U.S. tobacco market is still very robust, and the weakness in industry shares has been driven more by sentiment than by fundamentals. Whether that will continue to be the case given the threat of severe new regulations and potentially accelerated volume declines due to alternative products is certainly up for debate, but those are topics for another post.

Both the author and clients of Fortune Financial Advisors, LLC own shares of Altria.